This has been a year few us will ever forget - and there is still a month to go! The number of unexpected turns and twists is almost innumerable. "Work from home" became a reality quickly followed by an aggressive market sell-off in equities, suspended commodity demand and a general risk-off vacuum. Crude oil traded negative (?) for the first time. However, the bounce in both equity and commodity markets had been sharp since April while scaring participants with selloffs to start the fall. Entering the US election markets seemed to be turning down, again taking crude oil with it given waves of COVID growth globally, but the market rallied surprising many.

Something new, something old, something borrowed, something blue….

There is a lot going on at Auspice. A new and innovative fund, new people, new clients and growing assets.

Last month we talked about leverage, and the power of using this to gain cash efficient market exposure. Ultimately this led us to the launch of a new fund.

The Auspice One Fund combines exposure to traditional assets and the award-winning Auspice protective strategies on a near equal basis. It recognizes the powerful opportunity to benefit from the non-correlation of equity, fixed income and the divergent, negatively correlated strategies we specialize in.

Cash efficiency, the power of leverage and a new Auspice fund

Often, we hear that investors are nervous about the use futures contracts in investment portfolios. We are perplexed by this given this is a very powerful investment tool that is very common in institutional portfolios.

Futures have many benefits, including transparency and liquidity, but perhaps the most important is the cash efficiency aspect. Given futures have inherent leverage (the investor puts up a small percentage of the contract's value on margin), the cash can be used for different purposes, to generate income or some other uncorrelated investment. As such, you have more flexibility and get to decide how to deploy the cash.

Back to School

Thinking back to my youth, I remember that going back to school was an exciting and stressful time.

It was exciting to see old friends and get back into a routine and have some new social interactions. It opened a new chapter, with new activities, sports, and classrooms. The teachers were also excited and made you feel welcome. Parents were encouraging, excited and supportive of the whole process. But it wasn’t all rainbows and unicorns. I also remember being scared as hell. Some kids may have had their friends, but you weren't necessarily part of their club. It wasn’t easy to make new connections. In the end, you relied on your old trusted buddies to make new introductions and show you the way.

As I transitioned to the financial business, the "Back to School" phenomenon also existed. After a summer of less routine, quiet interaction and less networking, the fall was always a chance to look for new business opportunities and move existing business forward. Markets typically get a little more active and volatile as people tend to their investments, and financial and commodity markets react. Seasonality plays in as harvests, drilling and mining programs kick in creating transactions and opportunities after a period of summer doldrums. Getting together with your core relationships often leads to new ideas and expanded networks to explore for business.

Now imagine what it’s like for kids this fall: The kids will be segregated, masked, and shuffled leading to less interaction and much less personal development. Can you recognize a face behind a mask you have never met? The teachers will be under enormous pressure, and parents are worried on multiple levels, and a lot of activities and sports are curtailed or cancelled completely in many jurisdictions.

For business the same back to school excitement comes rife with unknowns in 2020. Is the company sound and able to survive? Will you still have a job? Is business moving forward and can you attract new business in this environment? To be sure it will be less personal, and a more zoom-driven time. How to capitalize?

Where existing relationships are present, I believe we will lean on them more and more for comfort and hopefully also referrals. We already know each other and talking by phone or zoom is remarkably efficient. But growing new relationships will require new ideas, novel efforts and the leveraging of your existing networks.

After all, how do you meet new friends as a kid? Often through your existing ones.

Remember that.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Business as Usual

July marked a seemingly big change for Auspice as we announced a partnership with Walter Global Asset Management (WGAM). While a minority stake, it is a significant step in many regards. As previously stated in other communication, this is a strategic relationship that respects our brand, culture and entrepreneurship and is anticipated to accelerate our growth at a critical time of opportunity. This brings expanded global relationships and distribution channels for existing products along with continued innovation and new fund launches while allowing us to maintain our focus on portfolio research and investment technology.

It is essentially, business as usual with an expanded group of highly capable team-mates that have a vested stake in our continued success.

But what is "business as usual" during these abnormal times?

Few things are normal in 2020. The year started with a US drone strike that killed an Iranian General, intense military tension, the "accidental" downing of a civilian aircraft in Iran, an impeachment trial of a US President, and Brexit. That all seams a distant memory next to the global “COVID” pandemic that started in China and seemed so far off to North Americans and Europeans. And then lock-down hit…

Since March many of us have worked from home, couldn't travel abroad, and this caused many business and social services to shut down. The word "Zoom" took on a different meaning. Many of those business have not and may not ever re-open. Economically, it has been devastating to many albeit aided by unprecedented government stimulus and support. For many, it has been mentally challenging which will have implications and social consequences for years to come.

But for Auspice, we continue to do what we do. We are generally unfettered by the confines of a physical office and this current period proved it. Moreover, on top of completing a major transaction remotely, we have seen in-flows into our investment strategies as investors look for uncorrelated absolute returns.

So, while partnership brings some minor changes and the environment has brought unusual market dynamics, what we do has not changed.

We see the environment as an opportunity to provide our investors a non-correlated and hopefully protective return stream when it is most needed as we have done in the past.

We aren’t doing anything different - it is business as usual.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Partnership

At Auspice, this month marks a big step for us. We have taken a leap that has been in the works for some time, forming a strategic partnership with an exciting firm with great people. While we have considered this type of a union a number of times, we had never found the right fit. As we went down this path with this partner to be, the choice became more obvious and confidence inspiring.

As an entrepreneur, the core of your being is stepping out on your own. In the beginning, you are ready to "go it alone", taking ownership of all the successes or failures to follow. It’s about this point one realizes that this can be a lonely pursuit. No one knows who your new company is, as they don't recognize the brand, even if they know some of the people involved. You may commit to doing something unique and innovative which attracts interest, but there are few opportunities for "partnership" in the beginning.

Even in pre-COVID times, there was a lot of isolation as an entrepreneur. As an asset manager, many of your clients are in other cities or countries. Historically, relationships take years to develop - many meetings, a lot of hotel and plane time. As such, collaboration with clients often takes on a special meaning as it not only tries to solve a problem, but it connects you to the client on an emotional level - a common purpose. We have often expressed our focus on client relationships as key, taking great pride and we view these as partnerships.

You quickly realize the value in having partners in many other regards. It could be for distribution of your good or service or help with expertise outside your focus (eg. marketing and sales). You seek this out and often time find ways to "work with" other companies for mutual benefit - perhaps managing and promoting a product, each doing their part. However, this type of partnership is not the same as one that has an equity stake and vested interest in your long-term success. Even once your brand is established, industries are riddled with bias and barriers based on size, track record, geographic location and clientele. Getting past this takes time and perseverance.

To find a partner that recognizes the challenges, can see the opportunities and wants to put their skin in the game for our combined success, is both affirming and gratifying. It’s a bit like finding the missing piece of the puzzle you started.

We are fortunate to have found a partner whose goals are aligned with our own. We still have the same energy and drive to succeed, but now we have a partner that can help us take Auspice to the next level. Stay tuned for an exciting announcement this week.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Remain agnostic. That’s the job.

Mostly, headlines are noise, and if we’re smart about it, we have all learned to filter. They are after all, designed to grab your attention. You become immune especially in light of the current volatility, economic and pandemic related reality. But every once in a while, a headline just takes you aback. Moreover, when it is in your field of expertise, and the focus of a company you founded, sometimes you take exception.

We have long believed that investment decisions should be driven by the facts. In the case of a quant manager like Auspice, we focus on return drivers like trend and momentum aspects. Is an asset rising? We may be interested in buying. Is it falling? We may short it. Basically, we divorce ourselves from market fundamentals and opinion, especially "popular opinion" as highlighted by media. If we "stick to the facts" we are able to provide a non-correlated return stream that is accretive to an investor's portfolio and ideally outperform in times of volatility and crisis. That’s the job. We do what we need to do to remain agnostic. We don't fall in love with ideas or investments. We don't love crude oil more at $30 than $50 to justify buying it as it may just go to $0. Or -$37.

As such, when I read headlines like "Value Managers Fight Back - On the back of the worst quarter ever for value stocks, AQR’s Cliff Asness and others defend the long-struggling style.”[1] I can't help but laugh and be a little annoyed.

“Investors are simply paying way more than usual for the stocks they love versus the ones they hate, without that behavior being rooted in anything we can find that seems like a great, rational economic story,” he said. For patient value investors, that irrationality is ultimately good. “If we’re right, that’s exciting. We say timing is an investing sin, but we’ve also said we can sin a little at true extremes. We don’t know when, but we believe value will come back, and be big.”

I have told investors that if I start injecting fundamental belief into how we invest or justify losses, it’s time to fire us. It doesn’t mean we don’t have opinions; we have many. For example, the commodity to equity ratio has been low a long time. But if we had tried to pick a bottom, simply on this relative value idea, we would have lost a lot of money. It has gone lower. For a long time.

For some, so called “value stocks”, have got very low priced, i.e. “great value”. Perhaps one could argue irrationally low, but I am not one to say. If they have been falling for so long, the real opportunity loss is having not shorted them. That would be the rational and agnostic thing to do if the goal is to “make money” versus fall in love with a story. One that can stay irrational longer than one can stay solvent.

Stay agnostic. Give us a call - we may have the right solution to help your portfolio.

[1] https://www.institutionalinvestor.com/article/b1lp9wzz1756nr/Value-Managers-Fight-Back?utm_medium=email&utm_campaign=The%20Essential%20II%2005192020&utm_content=The%20Essential%20II%2005192020%20Version%20A%20CID_b35d4a508d200c6d5857cde9893d6533&utm_source=CampaignMonitorEmail&utm_term=Value%20Investors%20Fight%20Back

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Be Bold, Be Cautious, or Both

Despite social distancing and working from my home office this month, I spent a lot of time talking to people. Ironically, more than normal. I talked to: family to friends, clients, both retail and institutional, current business partners, future business partners, and pensioners, as well as others from all walks of life: many entrepreneurs, teachers, doctors, dentist, farmers, loggers, mechanics - the list goes on.

Many of these people wanted to talk about investing. Perhaps some because we did so well in March and Q1. The question was often "What should I do now?" or "When do I step in back in?".

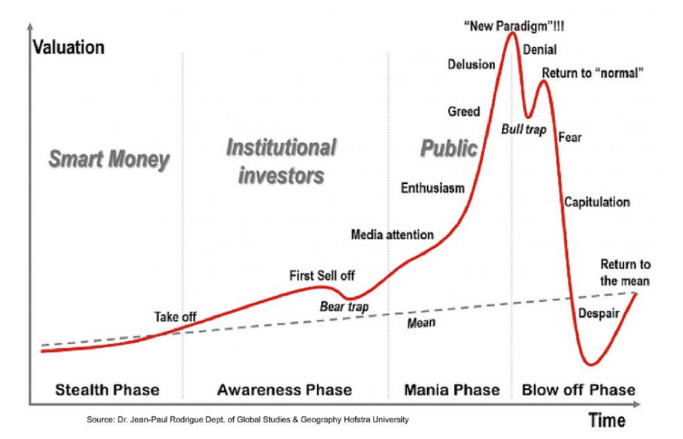

The thing that struck me was this: The fear of missing out. It is clear most investors want to take advantage of the depressed market in some way. They seemed (surprisingly) comfortable being bold. Perhaps this is muscle-memory from a decade of buying the dip and. Perhaps that is a good strategy again here. But when?

If the chart above doesn't scare you, it should. Where are we in the cycle? The bounce back in equities is shocking – Is the market really in better shape than it was half-way through 2019 when the market rose 29% (SP500)?

Emotions are key here, and very few people could say this isn't an emotional time in some regard. To some degree, the markets are just the result or manifestation of human emotion. As such, risk management is key. If you decide to step in, don't do it without protection. It’s akin to wearing a seatbelt. The volatility at this time is unprecedented and can make a good idea turn into a bad one rather quickly. You can close your eyes, but if your retirement savings are on the line, I wouldn't recommend it. It’s a time to be cautious.

This advice applies to governments too. If you are heavily dependent on oil revenues - the opportunity to hedge is gone. But if you are formulating a plan to rebuild, it should include risk management and this includes having a hedging strategy. Building a stronger economy through diversification of revenue sources alongside risk management will create a better ability to budget and forecast. It’s a lot like building a stronger portfolio for retirement.

For an investor, it may be prudent to build a stronger portfolio. A good way to do this is by combining non-correlated strategies. Finding those strategies that will perform well in both bull and bear markets while carefully managing the downside risk. Upside opportunity, with downside protection.

My advice is to be patient. You can be bold if you layer on a bit of cautiousness. I.e.. You can be both.

My last advice: give us a call - we may have just the solution for you…

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Weathering the Storm – True Crisis Alpha

The combination of the global health pandemic, equity and commodity correction, oil war and business shutdown are extraordinary. The gravity of this situation and the follow-on implications are difficult to comprehend. How does one weather the current storm and prepare for what comes next?

Equity and Stimulus

The amount of stimulus implemented by global governments and central banks is unprecedented. Trillions. Yet, will it matter? Some believe it will and the equity market will bottom and rally sharply to new highs. Many feel it will be largely inconsequential given this is a health issue and improvements in the war on coronavirus will be far more stimulative than economic incentives no matter how great. The reality is the economic implications for asset prices is difficult to determine with so many unknowns. As such, we believe there remains significant downside risk for equities. Given that the Q1 correction of 20% (S&P500) merely takes the "top off" the rally, the market is still higher than where it closed at the end of 2018. Are we better off than we were at the end of 2018? We don't think so. Moreover, we surely know it is far more volatile. Anything could happen.

What are the safe havens?

When we look for safe havens, the bond market has generally made sense. In March. after selling off in tandem with the equity markets, bond prices have indeed rallied. However, this safe haven status is related to the credit status of the issuer, often a government, and even this may be a concern going forward. Given the extent of stimulus and thus low rates (in some cases negative yield), the investment opportunity for traditional fixed income sector has been compromised to say the least.

While many have viewed gold as the hedge or safe haven, I hope this has been debunked. What is it anyway? Commodity? Currency? Some say "now is the time" but I say, where was the protection when needed as equity dropped 30% in the first two weeks of March 2020? Bouncing at the same time as the stock market doesn't make us feel much better in the last two weeks. Yet, many argue that now that the commodity shock has occurred, gold has the ability to act as an inflation hedge. To that we say, maybe.

Inflation

Given low interest rates and relatively strong US dollar, many believe there is a low risk of inflation. In normal times we would agree. However, we believe there is significant risk of unexpected inflation, the worst kind, from here. "Wartime finances that balloon budget deficits that are covered by money printing have proved inflationary through history." Per Julian Bridgen at Macro Intelligence 2 Partners, “...we are now entering an era of monetarily financed fiscal policy, just as the trend to de-globalization accelerates. This is going to be very inflationary”. Moreover, we fear supply chain disruptions may have significant implications for prices of goods. Given commodities are at extraordinarily low levels, there is a logical risk of higher prices due to lack of supply.

We believe a far better bet is spreading that opportunity for commodity appreciation beyond gold. Tactically, you want to own what is moving higher and in doing so it helps to be agnostic to what it is. Perhaps it is grains because of food costs, metals such as copper indicating the economy is picking up, or perhaps energy starts to rise after a 50-60% haircut exacerbated by an OPEC market-share war on top of demand destruction due to COVID-19. These are very real risks that affect the pocketbooks of individuals and companies alike. Real inflation.

Given commodities generally started to sell off in early in January and look to have been the "canary in the coalmine" of the global economic engine, is it possible they start to react to increased activity and/or a lack of supply quickest? While this depends on the market, it highlights one of the core benefits of commodities as a diversification tool: there is a ton of diversity within the commodity sector itself.

Portfolio Diversification

What the sell-off since peaking February 20th has reminded us, is that in times of crisis driven by incredible forces with deep economic implications, many assets become highly correlated. We have seen equities fall alongside commodities and many typical alternatives including private equity, infrastructure, and even real estate. Many of these assets are considered "diversifiers" for a portfolio, yet time and time again we realize that in during stress they do the same thing. The reality is that the entire rally over the last decade has been characterized by a low volatility grind higher followed by the odd, quick correction and subsequent recovery. This has happened over and over again. This is what convergent return streams do. There are few asset classes that counterbalance this given few are divergent (see graphic at side and definitions below).

Definitions:

Convergent return streams are characterized by many small gains with occasional devastating losses. Typically, the upside volatility is low while downside volatility is higher (negatively skewed with positive returns). Strategies are often based in fundamentals given the human tendency for logical sense. It is a “human” feel good strategy that gives investors constant gratification. Most active and passive investment strategies and alternatives fall into this category and behave like equities even in crisis.

Divergent return streams are characterized by many small losses with occasional big wins. Typically, the upside volatility is high while downside volatility is low (positively skewed with positive returns). Strategies are often non-fundamental and based in repeatable rules-based process and are agnostic to market direction or asset type. This return stream may at times feel “inhuman” without constant gratification, alike paying a premium. Returns are most commonly derived from trend following, common among CTA/managed futures/quant managers and may show up as “crisis alpha” at times when convergent returns are suffering.

One of the few asset management sectors that are indeed divergent historically are Commodity Trading Advisors (CTAs). These are managers that are agnostic to market direction, participate in all markets both financial and commodity, with the goal of providing a positive, but non-correlated return to a portfolio. Some call them "Quants" as the investment strategy is typically scientific, unemotional, risk management based and ideally negatively correlated at the right times. This is often referred to as "crisis alpha", the ability to earn superior risk-adjusted returns during crises.

However, this isn't happening for all CTA managers. Those who became enthralled with keeping up with the overvalued equity market, adding more equity and financial exposure in general have not performed well during this recent period. The “crisis alpha” expected from many CTAs has not shown up. Benchmarks representing CTA managers were down in 2018 as markets corrected and are again down in Q1 2020.

Auspice has a history of performing at these times of need dating back to our inception in 2006. Our outperformance has again shown up 2020 as true crisis alpha and we are working hard to make sure this continues.

The volatility and unknowns are likely to bring about many more surprising trends. This will occur beyond equities in currencies, bonds and especially across the diverse commodity sector. This will likely provide a series of opportunities for our disciplined approach. We anticipate this period lasting for the rest of 2020 and into 2021. We are very excited to help you weather the storm. Please feel free to reach out for more information.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

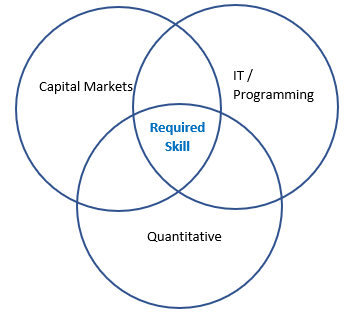

Investment Manager of the future

What skills does an Investment Manager need? I get asked this question a lot from investors, academics, and aspiring financial professionals.

As I started my career, the focus was on gaining a broad fundamental capital market experience. When combined with some basic economics, this formed a solid foundation for market participation. The TD Securities Trading development program, which is where I started my career, rotated "associates" through money markets, bonds, and currency desks, and if you were fortunate, also commodities and equities. It was a great base to build upon. Thereafter, the goal was to specialize.

It became apparent to me that while fundamental knowledge was a great base, it was quantitative skill that was needed to really progress. Quantitative skill allows you to apply scientific method, to create and test investment trading and investment ideas. It enables one to remove the emotion from investing, thereby reducing cognitive biases that humans are prone to fall prey to. This combination of fundamental capital market understanding and quantitative skill, which is then wrapped in a layer of risk management, was a powerful combination.

But it isn't enough anymore.

The last necessary skill is the ability to efficiently code and automate these strategies. This goes far beyond the excel spreadsheet most have associated with quantitative skills in the past. Programming theories and strategies alongside the ability to interface with execution systems from brokers and exchanges, pulling data and reports from vendors, managing databases is now mandatory for any company that wants to compete in the space. The ability to communicate in multiple (programming) languages is far more valuable than multiple spoken language.

While each of these three skills are valuable on their own, it is the combination that provides the powerful skill-set required to compete and thrive in the modern markets. Capital markets experience may help you service a client base in basic way, but that has been replaced by quantitative skills. The fact is that rules-based, active management wrapped in discipline will generally outperform and can be employed at a far lower fee given less people and traditional infrastructure costs. Meanwhile the lonely programmer has discovered a purpose!

The investment manager of the future needs market understanding, the quantitative skill to develop investment strategies wrapped in rules-based discipline and have the IT capabilities to employ them efficiently.

We are happy to discuss how the intersection of these skills can help you with your investment portfolio. Give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

The opposite of love – and the markets

A colleague recently asked me, as we were talking about the energy industry, "what is the opposite of love?” Given the struggle and lack of performance in recent years, my immediate thought was people either love something, or they hate it. This is observable in many aspects of life: I hate this football team; but I love this one. I hate this politician; I love that politician (Not!). And while it feels like people hate the energy industry right now, he disagreed, and his response had me thinking about this ever since.

While most people talk in these extreme terms, perhaps for dramatic effect, the reality is most people act in a far less committed way. Most commonly they just accept or ignore the way things are. They are indifferent. This, my friend suggested, is the opposite of love.

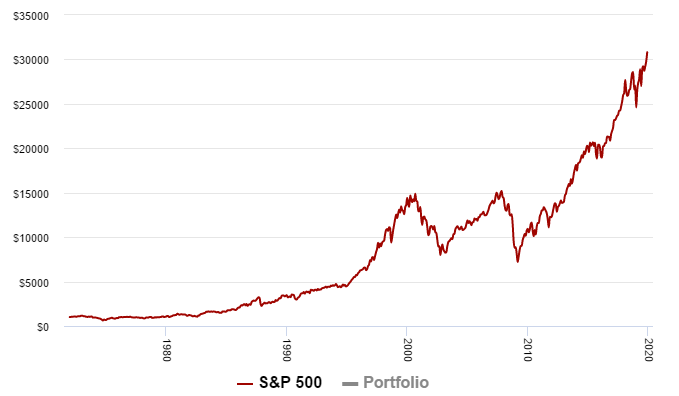

For the stock markets, the bull market we are in has been called the "most hated bull market in history" by some. Not without merit. While the scare in 2018 had investors withdraw $200 billion to end the year*, it is estimated only $198 billion came back in 2019 despite the market roaring back, posting one of the strongest results in history. This brings the S&P500 (total return) to 8.8% annualized since 2007, even including the 50% plus pullback in 2008. Incredible. What’s to hate?

I don't think people hate it at all. At worst they may be feeling they missed out on an opportunity if they didn't participate. Perhaps, the constant fear mongering that the markets will inevitably correct, constantly bombarding investors has made investors numb to it. And they have become indifferent.

But here is the scary part. While no one knows when it will happen. It is inevitable that the markets will correct. That is normal behavior. If your exposure is only to the stock market and other correlated investments, you are at risk. While diversifying into other things make sense, do they help when the market drops? Indifference to this reality can be very unpleasant indeed.

Fortunately, the remedy to indifference is quite simple – it’s action.

It’s up to the Energy industry to take action to get the right message out about the industry with respect to climate, environmental and its positive contribution.

It is up to you to vote in a democratic society. It is up to you as an investor to make sure your portfolio is protected from inevitable downturns - so you can worry less and just enjoy life.

Can you possibly do better than the incredible S&P 500 returns? Yes.

Hypothetically, if you added 20% of a Diversified Managed Futures strategy (like the one Auspice manages) to the S&P 500 in 2007, you not only have a slightly better annualized return at over 9%, and a better risk-adjusted return as measured by a better Sharpe ratio. Moreover, that 50% pullback is now 35%, and volatility has dropped by 24% (on a relative basis). Better returns, and a reduction in risk.

Don't be indifferent.

We are happy to discuss diversification and products that may help your portfolio. Give us a call.

*per the Investment Company Institute regarding mutual and exchange-traded funds

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Commodities and Careers in 2020 – I have been here before

While history doesn’t necessarily repeat, it often teaches us lessons about the past and flows of human interests including investments. 2019 can be remembered by a year of geopolitical tensions, global trade and macroeconomic issues, rangebound commodity prices (until a late year rally) and an undeniable stream of climate change claims to sift through. Note this too has been topical before as I remember a university friend wanting a recycle symbol tattoo on his arm circa 1995. Not sure if he ever got it but he did end up in the oil and gas industry.

I started my career in 1995. TD Bank recruited at the University of Calgary for their “Trading Development Program”. I was very excited as I went into business school wanting to learn about trading. I literally had to borrow a suit for the interview as my existing suit was not very business-like (more “Night at the Roxbury”). I was ecstatic to be offered the job in my fourth year and moved to Toronto the following summer to join the program in August 1995. It was an exciting time as the stock market was roaring and the “Dot-Com” boom was on. After much of the year in training, I was offered a role on the money market desk - a great win for anyone on the program. But what happened next changed everything.

As luck would have it, TD lost their energy and commodity trader. I was asked what I knew about this area given I was the “kid from Calgary” with a farming family background who wore cowboy boots on Fridays. The honest answer was “not much” but was very interested. I was offered the job and told “the world is your oyster” by the global head of trading. I was elated but the others on the program and my new friends on the trading floor reacted far differently. Many thought I was throwing my career away. As far as they were concerned, commodities were so far out of favor they were dead. It was about tech stocks and the " 'net". And for the next 5 years they weren’t wrong. The boom continued until 2000 when the market peaked, but by that point I had already made my second surprising move - I left in 1999 to join Shell Oil’s trading division right as oil was $11/bbl. Again, people said I was throwing my career away. My thought was “do you think oil stays at $11??”.

It didn’t. Moreover, the stock market began a much-needed correction in 2000 and commodities were the place to be for the next decade.

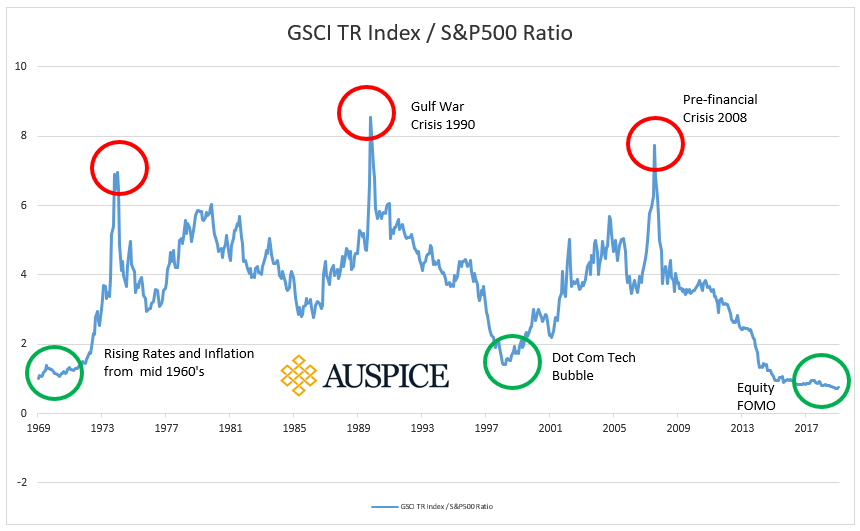

It is now 2020 - but I have been here before. The commodity to equity ratio has never been this low (see chart) and it is commonplace to hear of commodities being irrelevant and naively being removed from some asset allocation models.

But here is what I know - commodities have never been more relevant than today. The need for materials including petroleum products (in almost everything), metals, agricultural for foods and other soft commodities is not miraculously going away. It is foolish to think it is.

This is the important part - while the world continues to grow and want things, the supply side has got harder, more expensive, less profitable and thus less focused on. Capex is down in most commodity sectors. ESG themes have made things more challenging and expensive regardless of your stance. Could we have a supply crunch? I believe it may be upon us.

As a commodity tilted (not exclusive) manager, we are biased in one sense but truly putting our money where our mouth is on another. Others agree.

On November 25th (Reuters), Goldman Sachs said its top 2020 trade recommendation is to be long its commodities index, with the best returns likely to come from oil, reasoning that a decline in overall capital expenditure would in turn result in reduced supply. .... a "sharp and visible drop" in capex. Link here.

While we don’t have a crystal ball and know exactly what markets will go where, we believe it will likely be an increasingly volatile marketplace due to global economic unrest, an upcoming US election, a massive Chinese economy, discourse in Hong Kong, and trade unrest with the largest players. Commodities will be included in this volatility.

This sector has been called out before - typically at the bottom. And unless you have found efficient ways to make cellphones and batteries from pixie dust, pilot planes and ships on solar, or grow all your food in your home, commodities are what make this world go ‘round...

We are happy to discuss diversification and products that include commodities for your portfolio. Give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

What’s a normal pullback for a bull market?

How does one navigate a market that seemingly goes up at a 45 degree angle, with low volatility, for a decade? It’s not like it hasn't happened before - from 1990 to 2000 prior to the dot-com correction, the S&P500 grew at 13% annualized with a 16% pullback - very similar to the current run from 2009 at 12% annualized with a 17% pullback (peak to trough monthly). Eerily similar. While we know that corrections are inevitable, we tend to ignore this risk during great runs. Will it be 10%? 15%? 20%? The correction in 2018 was 20% to the day. Was that enough? Look at the chart - what do you think?

History shows us that we can expect 40-50% plus from time to time. While some may argue that those times (2001 tech or 2008 financial crisis) were driven by specific events, we can't disagree. But here is the thing – the cause wasn’t obvious until the dust settled. And we don't see the next "event" any different. What will it be this time? Or what are the risks and catalysts?

Recent bank (repo) liquidity crisis?

US election uncertainty that could change tax and financial policies?

Slowing global economy and trade concerns?

Manufacturing PMI at recessionary levels?

Delinquencies rising in some retail areas such as auto loans?

Valuations of stocks now believed to be higher than prior to Tech bubble and the end of the roaring twenties?

Massive Corporate debt?

How does one protect themselves from the downside risk? One way is to do what Ray Dalio has done recently at the world’s largest hedge fund. Bridgewater has made a $1.5 billion dollar bet stocks fall by March 2020 by buying put options that will pay off if the market drops precipitously. This is one option.

Another way to protect the downside risk is with diversification that lasts longer than the near term. One of the best diversifiers to an equity tilted portfolio is Managed Futures. The correlation is low and generally negative when equities are selling off causing performance at a critical time. In 2008, our flagship portfolio added over 44%.

This is what we do at Auspice. Give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Alternatives are no longer alternative

In October I attended an institutional investor conference in Toronto that reminded me about the significance of alternative investments. It used to be that these were fringe discussions, on the cutting edge. Even the name "alternative", conjures up visions of something edgy or rejecting the mainstream. Alternative music, alternative lifestyles, alternative energy. When it comes to investing, alternatives are still considered by many retail advisors to be a non-mainstream choice. Fast forward a few years, and now many in the institutional space consider alternatives to be part of the mainstream.

This acceptance seems to fly in the face of the pitch of old for "Alts"; that they generate higher returns by taking greater risks along with the potential benefits of low correlation to more traditional assets like stocks and bonds. Alts were considered sophisticated and opaque, adding to the exclusive allure.

When looking at institutional investors, we generally consider them a group that has the role of protecting capital first and foremost, while also looking to achieve investment goals. In practice, this is often the case for groups like pensions, and endowments. These groups realized many years ago that they needed to look at alternatives to achieve return goals along with the goal of reducing the stock market risk as asset allocation became their focus. They were early adopters of investing in private equity, infrastructure, real estate and these are now considered "traditional" alternatives. These three categories alone often make up nearly 50% of institutional portfolios. Adding "hedge funds", now often referred to as "absolute return", rounds out the typical institutional Alt focus.

These strategies have now found their way into retail portfolios in varying degrees. Given interest rates are very low and the stock market has rallied for over 10 years, the challenge of finding new reasonable returns at modest risk is becoming more challenging for institutional and retail investors alike. While the cost and complexity of alternative investments has always been a criticism, efforts have been made provide lower cost solutions via delivery mechanisms that all investors can access including ETFs and mutual funds. Many alternative strategies that historically were structured with hedge funds like fees of 2% management fee and 20% performance sharing are now available for management fee only to meet investor and regulator needs.

While some global retail markets have embraced alternatives, looking to invest more like the institutional investors, some markets have lagged. While Europe and the US have been very progressive, with a system of many independent RIAs (registered investment advisors) acting like mini-institutions and employing the same philosophies as the respected Yale endowment model, Canadian investors are indeed behind. Most retail investment, largely controlled by the Canadian bank monopoly, has provided little in the way of alternative solutions. As of 2019, this has started to change, with the advent of a new regulatory framework for liquid alternatives in Canada – and not a moment too soon.

To quote the CEO of one of the largest Mutual fund companies in Canada:

The democratization of alternative investments has just begun in Canada with the increasing availability of “liquid” alternatives – funds that make use of hedge-fund-like investment strategies – which debuted in January for Canadian retail investors. Prior to this, they had been mostly within the domain of large, sophisticated institutional investors, such as public pension plans, sovereign wealth funds, endowments and foundations, and high-net worth individuals. - Barry McInerney is the President and CEO of Mackenzie Investments

To learn more about the innovative Auspice alternative investments and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Trading and Living are Episodic

As I left the office Friday Sep 13th, I spoke with my Auspice co-founder about something I read describing good trading as "episodic, not continuous". It was a brief conversation as we both agreed that this is indeed the case. Ironically, this occurred hours before Saudi Arabia was hit by drones and cruise missiles, disabling over half of its oil production and sending oil soaring in its biggest one day move ever. It reminded me of an adage in energy trading: never go home short before the weekend.

While it is human nature to want constant gratification, it is a dangerous way to trade or invest. Opportunities in investing are not constant or consistent. The challenge is that good opportunities are often few and far between. They require patience and discipline in order to be prepared and engaged enough to recognize the opportunity when it appears. Moreover, you need to have the capital and structure to invest in place as these are often fleeting opportunities.

To deal with many aspects of episodic living, managing the bankroll is critical. This is the reason good poker players often fold, knowing the odds are not in their favor. Given one of the most critical aspects of the game is to manage the capital pool, betting when there are good odds on a rare hand is critical. Good players do not bet without these odds and they are not betting all the time. Moreover, you can't bet if you have no chips left or make a decent size bet when odds are in your favor.

Did we make a bunch of money post Saudi attacks on September 16th? No (although the CCX ETF rose 18%). Did we lose money? No. Job #1 is to manage the capital pool. Job #2 is to wait patiently for opportunity. Opportunities like we experienced in August are rare. Without taking any atypical risk it was one of our biggest months in history, providing offsetting returns as stocks, commodities, currencies and rates all moved sharply.

At Auspice we remind investors: we don't make money every day, month, quarter or even every year. We aim to make money when it counts and when our strategy has an edge. This is often when investor's portfolio's need it the most as the traditional markets are falling or at very least experiencing volatility which is always unnerving. Returns are not continuous as opportunity is not continuous. Opportunity is episodic - and that requires patience and discipline.

For more about the innovative Auspice quantitative CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Special Teams

A common analogy used to explain what our funds do is an insurance policy. Investors, and in particular retail advisors, found this explanation comforting given the history of paying out in times of "market crisis". It perhaps also explained why during the low volatility, grinding higher good times of the equity market, that CTAs may not perform nearly as well, often making investors question the value at precisely the wrong time. I have never liked this explanation albeit admit to falling into this discussion trap more than once.

I prefer to describe what we do as Special Teams. This analogy seems to fit far better and was affirmed to me earlier this month as my son started football (American/Canadian style) and the market started to get volatile.

While insurance implies a guaranteed payoff that only occurs after an event or crisis, this is not what we do. We are not the same as buying S&P puts to protect the downside - a perfect negative correlation. Rather, we employ a strategy that has the potential to benefit during volatility, from more than just equity (includes Currencies, Interest Rates and Commodities), but also has a positive expected return over the long term. Insurance does not do this - at the end of the day, the winner of the insurance game is the insurance company - just ask Warren Buffet.

Special Teams have a similar but different function - they are relied upon at critical times to complete a task, put up points or protect field position. The goal isn't to only show up in the "clutch", but to be called upon as special players who also often hold other roles. Their value is positive, and their important contribution is significant to the outcome of the game.

Do we show up at key times? Yes. Do we contribute positively over time? Yes. Do we keep up to the returns of the stock market all the time? No. We aim protect your asset base and have the ability to add value at critical times of need.

For more about the innovative Auspice quantitative CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Thinking Big and Thinking Small

As I read morning headlines for July 22nd (Sunday evening), the first thing across my screen was that the "market bounce" first half 2019 had caught the massive Bridgewater hedge fund off-guard. Immediately I am thinking this must mean a massive loss, unrecoverable, and given its size ($150 billion or so), this could have implications for the markets in the weeks ahead. I continued on with my morning but had this in the back of my mind. I thought about it some more - wondering how a seemingly disciplined trader like Ray Dalio and Bridgewater could have a "massive loss" in this market environment. While I don't know all the inner workings, their philosophy is not unlike ours at Auspice. They follow trends identified in one fashion or another, with rigorous risk management.

Then I read the article where it is reported that Bridgewater Pure Alpha was down 4.9% to June 30. 4.9% - less than 5%. This mid-summer "wrong-footed" headline maker is a result of a less than 5% pullback as equity and bond markets have bounced back sharply after correcting in late 2018.

This is a perfect example of thinking small. Here is a fund that is non-correlated to the stock market making over 14% in 2018 while the S&P was down 6% and it starts 2019 by correcting a modest amount while the S&P rallies.

I encourage investors to think bigger.

Rates are dropping - historically this means the Fed is concerned about credit quality and the health of US institutions and this could help the stock market. However, critics contend that historical recessions stemmed from easy money credit bubbles leading to market weakness. Either way, it will likely bring a strong difference of opinion, which means volatility and risk taking. Typically, this is a good environment for quantitative asset/hedge fund managers and trend followers.

With a record-setting 11th year of economic expansion and rising stock markets, is the fact that a top performing fund manager was non-correlated and negative while the stock market rallied really the biggest worry? We recommend betting on those that made money when others did not historically. Think bigger.

For more about the innovative Auspice quantitative CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Getting Spoiled and Market Rodeo

“Nothing sedates rationality like large doses of effortless money."

–WARREN BUFFETT

This same sentiment appears in many aspects of life. If you give a dog a treat every time you come home, he expects it. If you give a teenager everything they whimsically desire, they become spoiled. Think of forced tips for waiters or (Canadian) provinces that gain transfer payments.

Like the old proverb, "give a man a fish and he eats for a day, teach a man to fish and he has enough fish for a lifetime”. Or the generous man who offers his dock to that fisherman only to learn the fisherman came to expect the access as a handout, for free. The truth is if you provide everything to a group of people or society for nothing, they come to expect it and lose appreciation for it.

Which brings us back to investing - and another example of this same psychology at play.

Periods of extraordinary or prolonged gains causes investors to have unrealistic expectations. They begin to discount volatility or even lose sight of the real risks and magnitudes. I believe this is where we are now.

This isn't only applicable to retail investors, the pros at institutions fall into the same traps - except bigger. For example, using alternatives is now commonplace. But which ones? The answer is often whatever has been the top performing recently and the most familiar. For example, equity hedge funds used to hedge equity exposure often ends in tears. The problem is that many “alts” have high correlation to the stock markets they are attempting to protect and this means added negative skew (downside volatility is higher than upside). Doing the easy thing has little political or corporate risk as everyone is doing it. Lots of small gains and modest yield feels good but comes at a price as eventually these markets converge and correct violently. Doing the right thing is hard and can be uncomfortable.

So while investors and commentators appear to be drunk on years of returns and dividends or high on Cannabis stock returns, I believe the reckoning is coming. And while I can’t see the catalyst through my crystal ball, and each time it’s different, one thing rings true: I have been to this rodeo before...

Let the Calgary stampede begin.

If you are planning a visit to Calgary during the Stampede or this summer, please let us know. For more about the innovative Auspice CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

On Pioneers and Innovation in the West

"Go West Young Man" …an often used cliché.

For me, it is ironic because the first thing I did, like so many others looking for a career in the markets and finance, was to go east. Whether it be New York, Toronto, or London - those are the destinations one often cuts their teeth in as they are the epicenters for trading, finance, market participation. These business centers are full of career opportunities no matter where you are from for a hodge-podge of "foreigners" who are ambitious, excited and willing to learn.

However, once you’ve been there a while, the opportunity seemed to shift. People often head back west. Why? What is it about the west? I liked the word so much that I named my son “West”.

I believe there is a spirit in the west that goes back to the pioneer days that endures to this day. There is an excitement of breaking new ground, trying something new and innovating that is germane to the west.

Whether it be in Houston or Calgary for Energy (for me I ended up in both), Silicon Valley and San Fran for tech and VC, or Seattle for software, payments and the online marketplace that is sweeping the globe, they are all in the west. The culture of these western locations and the businesses that develop there are built on innovation and disruption.

However, I also observe that much of the financial business has remained concentrated in the east. Perhaps it is the shear scale, concentration of banks or maybe it has been the focus of talent historically. Many of the FinTech hubs are in the east, but with the concentration now shifting to new locations out west. We have seen signs of this with Robo-Advisory firms like Wealthfront in California and Wealthbar in Vancouver. Or even in Calgary with Solium (stock options software) and Benevity (corporate giving).

The concentration of educated, ambitious engineers and computer scientists makes a difference. Places like Denver, Austin, Seattle, Calgary and Vancouver offer an educated and experienced workforce along with a lifestyle often sought by the creatively disruptive crowd. Engineers that once went into the ubiquitous energy business now have other options and other western locations to consider.

But here is my prediction - the same disruption and creativity we have witnessed in software, payments, electric vehicles, tech, and retail that developed in the west will also happen in financial services and markets. Given online technology and the ability to connect to exchanges anywhere, location is less relevant. The west will be a key driver of this shift as it has been in so many other areas.

If you are planning a visit “out west” to Calgary, please let us know. For more about the innovative Auspice CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.

Is there a real black gold?

Near Calgary, there is a town named Black Diamond. Everybody here understands the origin of the name given the history of oil production and the related economic benefits. But while diamonds are the metaphor, it is a commodity that is hard to understand and thus seldom considered in terms in a portfolio context. Gold is another story.

Together, gold and oil are talked about more than all other commodities combined. They were both amongst the first to become available to retail investors via exchange traded funds (ETFs). And while there may be diversification benefits to including either or both in an equity dominated portfolio, the need for each is not equivalent.

Oil has for some, become the vilified symbol driving climate and environmental efforts, this does not takeaway from its current importance. Oil is critical to running most aspects of our modern society, economy and trade. It is the most important energy source yet its use goes beyond transportation from health and medicine to electronics and textiles. From medicines like Aspirin and antiseptics to anything plastic, from water pipes to contact lenses. The list is almost endless.

As such, there is no doubt that oil serves a critical role as an input to most everything, yet it can also serve a purpose in a portfolio. Given its importance, the inflation aspect cannot be ignored and has been highlighted by central banks. Oil and Inflation are indeed correlated higher than gold.

Moreover, direct investments in the commodity (versus equities of producers) can have a beneficial effect. This has been argued with gold for a long time. There is no need to be an “oil bug” alongside the “gold bugs” to justify this – we can demonstrate the value.

The common belief that using gold as a proxy for all commodities is a mistake that is easily proven given the inter-commodity correlation is low. As such, adding other commodities may help, but adding oil is important. They don’t call it black gold for nothing.

For more about the Auspice CTA and commodity strategies and the potential portfolio benefits, please give us a call.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

Futures trading is speculative and is not suitable for all customers. Past results is not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to “Accredited Investors” as defined by CSA NI 45-106.