To download the Auspice April Blog as a PDF, click here.

This commentary is intended for general informational purposes only and does not constitute investment advice or a recommendation.

I began my career in 1995. People said I was throwing it away when I made my way onto a commodity desk in 1996 – it was the dawn of the internet, the Nasdaq was ripping, and commodities seemed “old school”. It was about bits and bytes, not bricks and mortar. Until it wasn’t.

We realized two things when the bubble burst: the new paradigm was here to stay, and commodities, which had been underinvested in for a decade plus, were needed. China was the generation demand shock, laying the groundwork for a supercycle that lasted over a decade. The 1970s supercycle had lasted just as long.

Two basic ingredients facilitate a commodity supercycle:

An extended period of underinvestment in commodity supply

A generational demand shock

Background

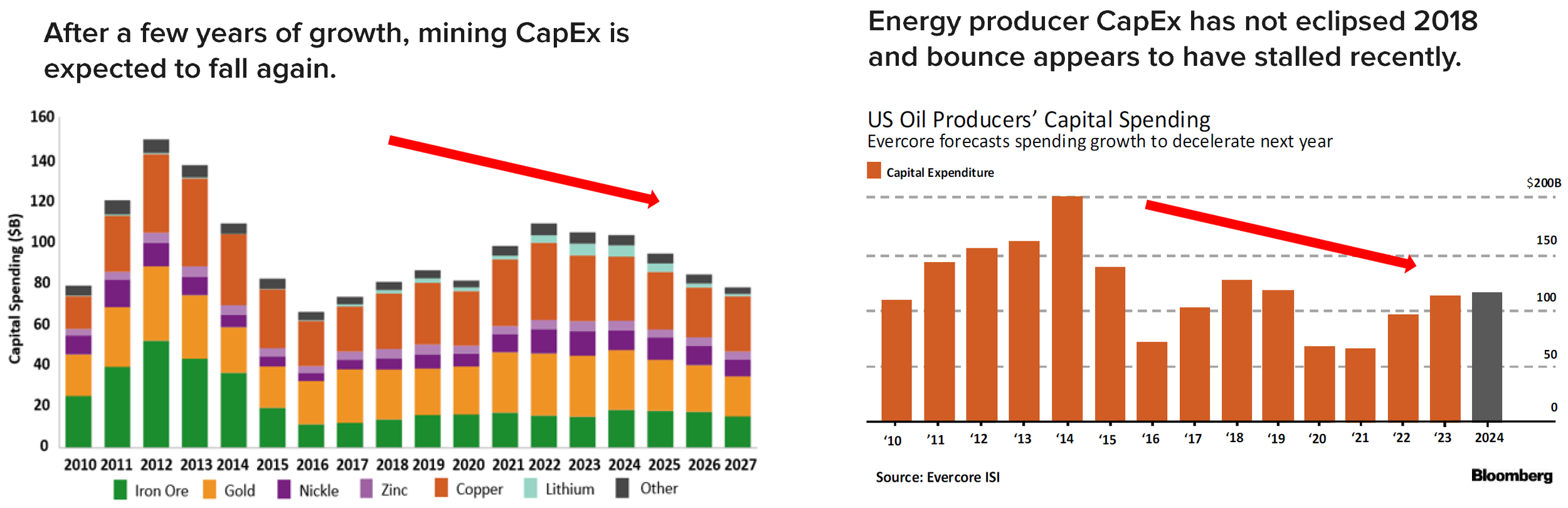

As we entered the 2020's, it was realized that after CapEx peaked in 2012-2014 in Mining and Oil/Gas, and it had not come back (See Chart 1).

Chart 1: CapEx 2012-2014 Peak

Beyond the pandemic itself, COVID-19 was a shock to the system. It accelerated the “Green Transition” conversation to “build back better” in both developed and emerging markets. The scale of that shift is visible in Chart 2 below: global investment in the energy transition has more than doubled since 2020, from $1.0 trillion to $2.3 trillion in 2025.

Consultants like Mercer1 put it bluntly: “Commodities will remain an essential component of the economy, and investors should note that there is no transition pathway to a climate-neutral world that does not involve commodities.” Pre-pandemic estimates already pegged the world’s infrastructure gap at $15 trillion by 2040, with calls for over $10 trillion in US green infrastructure alone2 - a gap that has only widened since.

The recognition of underinvestment across the commodity complex (not just oil) hit, and the start of a commodity supercycle began in mid-2020.

Chart 2: Global Investment In Energy Transition, by Sector

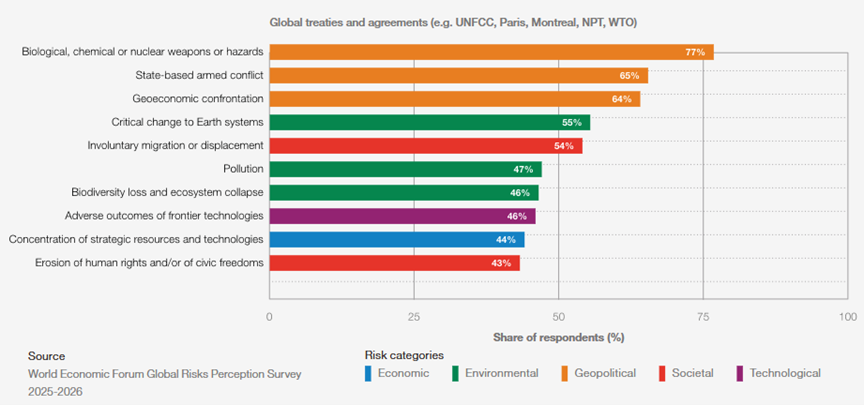

In the wake of COVID, the Russia–Ukraine war strained supply chains and regional conflicts erupted across the globe. Deglobalization - accelerated by the US and China - became more than rhetoric. The World Economic Forum’s 2026 Global Risks Report3 makes the shift plain: of the top risks global leaders want addressed by treaty over the next decade, the top three (Chart 3) are all geopolitical - weapons proliferation, armed conflict, and geoeconomic confrontation.

Chart 3: Share of respondents (%) Top risks addressed by global treaties

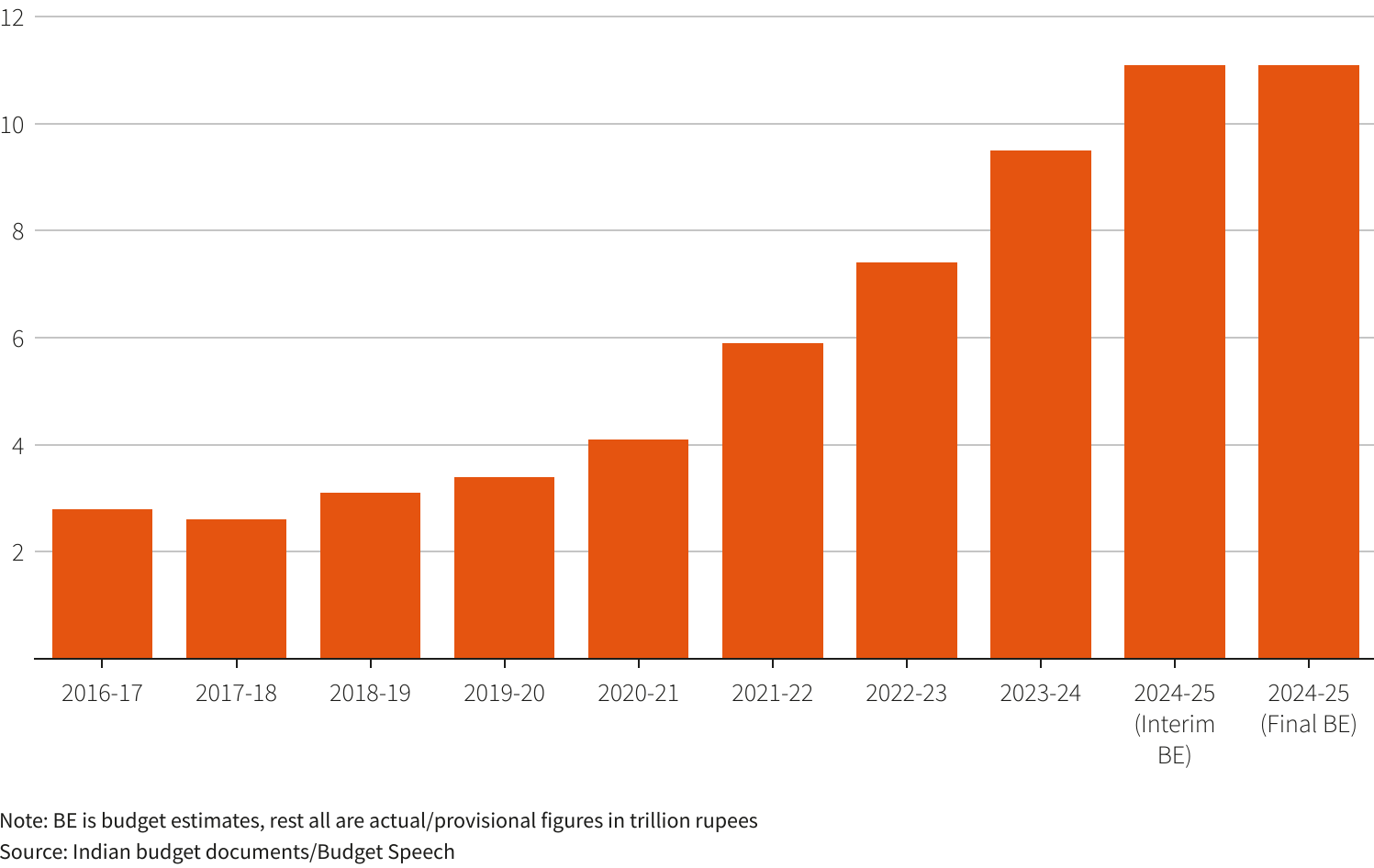

On top of this, demographics became a factor. By 2024, it was clear India had become more than just the world’s largest country at over 1.4 billion people. It had the fastest-growing middle class on the planet, currently third behind China and the US, but projected to take the top spot by 2027. Historically, it’s the middle class that drives commodity demand cycles

A country's commodity consumption is a function of population and income, but the relationship isn't linear. The real demand shock comes from the middle class, when countries spend to industrialize and urbanize. India's emerging middle class will drive demand for Copper, Iron Ore, Zinc, Aluminum, and energy needed to build modern infrastructure, cities, and the homes and industry that fill them. At the same time, India is shifting from a top exporter of key agricultural commodities to a top consumer - and the government has tripled CapEx from 2019 levels (see Chart 4).

Chart 4: India Federal Government Infrastructure Spending

This now formed what we called the “3 D’s”: Decarbonization, Deglobalization, and Demographics - see our special feature to the Financial Post for the inflation implications. To add salt to the opening wound, Western government (read Canada) policies have not been conducive to resource development, and Trump tariffs and structurally higher interest rates aren’t helping. Labour shortages and unionization have added to cost-push inflation - the kind central banks don’t have a lever for. Raising rates helps demand-pull inflation; it does not help with this. All of this forms the set-up for a long list of commodity cycle drivers, versus the early 2000s, when the single driver was China.

What’s Changed?

However, we now think we had something wrong. The factors have shifted again, and the supercycle effectively reset in 2025.

Why a reset in 2025? Because this is when the AI and electrification trade changed the landscape. Tech is bits; energy is atoms - and for decades, the conversation was always one or the other. Now they’re converging. It’s not just power and copper wire; it’s energy of every kind and commodities broadly. With this factor in play, we think the cycle could run 10 years from 2025, or potentially 15+ years from 2020. Either way, in our opinion, it may run longer than many expect.

We believe we may be in the early stages. The infrastructure required for AI and electrification is just getting started.

There's no denying AI is the game-changer of this era, just as there was no arguing with the internet in the late 1990s. The difference: this shift eats commodities4. As one industry analysis5 of AI's power demand put it: "Like all technologies known to man, AI has a dark side to it: high energy consumption."

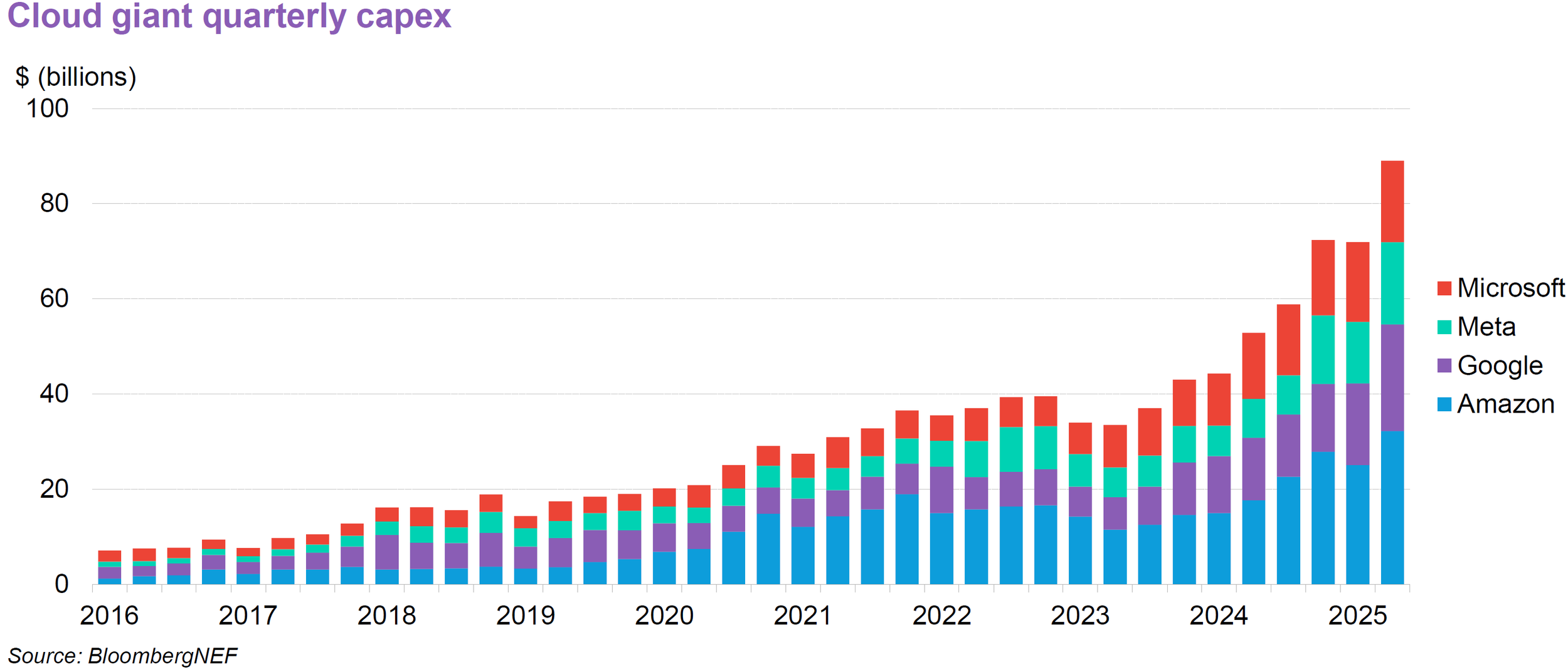

The link between commodities and the current tech boom is driven by demand for data centers, computer chips, electric vehicles, and batteries - and big tech is starting to act on it directly. In 2023, major brands including the investment arm of the IKEA group were already following automakers' lead, snapping up stakes in suppliers of raw materials and energy to secure their supply chains. In the first half of 2023 alone, more than $4 billion was spent by firms investing across food, batteries, chemicals, autos, mining, and waste and recycling6. Cloud giants are following the same logic on a much larger scale. Chart 5 highlights how quarterly capex across Amazon, Google, Meta, and Microsoft has grown from roughly $20 billion in 2020 to nearly $90 billion by late 2025, with much of it flowing into physical infrastructure: turbines, transformers, copper, steel, and the chips that sit on top of it all7.

Chart 5: Cloud Giant Quarterly Capex

At Auspice, we think big tech may be the next major commodity buyer, and they're moving in at a time when supply is already tight and prices are already rising.

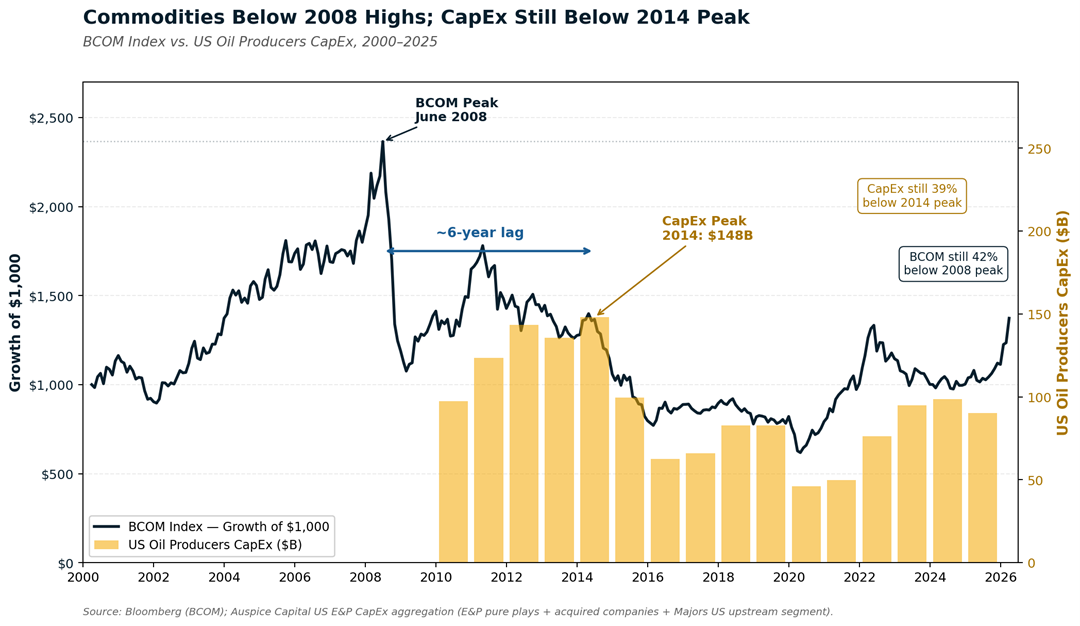

Commodity benchmarks haven’t even made new highs yet – the BCOM remains well below its 2008 peak (Chart 6), which itself was followed roughly six years later by the 2014 peak in US oil & gas CapEx. The lag from price peak to CapEx peak is built into the data.

Chart 6: Commodities below 2008 highs; Capex Still below 2014 Peak

Given the difficulty in getting projects started, let alone completed, we already thought this cycle would be elongated. Projects that historically took around 7 years now take 10 to 15. Uranium projects can take 25 years or more. The net effect: it will take a decade just to bring supply up to demand.

Other Factors

Demand for commodity diversification will add to the bid. Investors increasingly recognize that bonds don’t hedge equities in inflationary regimes (a hard-won lesson from 2022). Gold isn’t an inflation trade; it’s a diversifier, and increasingly a hedge against the US dollar itself as it devalues. We believe a normal inflationary environment (the 100-year average is roughly 3%, 4% since 1970) is here to stay, and that alone elongates the cycle.

We don't subscribe to the view that oil demand is falling sharply, and current data does not appear to support that outcome. And alongside oil, we see structural long-term demand for natural gas and uranium. The thesis is energy everything, and commodity everything.

The Israel/US/Iran conflict isn't just about Iran or uranium enrichment. The Strait of Hormuz is a chokepoint for almost every commodity that matters: petroleum makes the headlines, but natural gas, helium (required for semiconductor manufacturing), grains, industrial minerals, the chemicals used in copper and other mining processes, and the fertilizer that feeds an expanding world all flow through it. The strait is strategic, full stop.

A friend recently told me a story that impacted me greatly. He said you get three chances in your career: the first, you’re young and learning and just happy to be in the investment business - you see it but miss it. The second, you know what you’re doing, but you don’t have much money or access to capital - maybe a small benefit. The third is later in your career: you know a thing or two, have some capital, and see it coming - and shame on you if you don’t take advantage of it. This is how I feel about the commodity opportunity in front of us.

SOURCES

https://www.huffpost.com/entry/infrastructure-bill-biden-administration-progressive-democrats_n_605e518ec5b6531eed04e2a6

https://reports.weforum.org/docs/WEF_Global_Risks_Report_2026.pdf

https://www.bloomberg.com/news/articles/2024-01-29/blackstone-is-building-a-25-billion-ai-data-center-empire

https://oilprice.com/Energy/Energy-General/AI-Industrys-Power-Demand-Is-Skyrocketing-Globally.html

https://www.reuters.com/sustainability/companies-buy-into-suppliers-secure-deliveries-hit-green-targets-2023-07-21/

Data Centers and AI outlook for 2026 – BloombergNEF

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results. The views expressed are those of the author and do not constitute investment advice.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus or applicable offering document before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

All data is believed to be reliable but has not been independently verified.

The indices shown (Charts 1-5) are for illustrative purposes only. Index returns do not reflect the deduction of fees, expenses or transaction costs. Past performance is not indicative of future results. The referenced indices are not directly investable. Also, where ETF or index proxies are used, they are intended to approximate the performance of the underlying strategy and may not reflect actual investable results.

These materials are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. (the “Manager” or “Auspice”) makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the applicable offering documents before investing.

This material may contain forward-looking statements, which were prepared for the purpose of providing general educational background information and may not be appropriate for other purposes. Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to an Auspice managed investment fund (the “Fund”), where applicable, and the Manager. Forward- looking statements are not purely historical facts but reflect the current expectations of the Fund, where applicable, and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s, where applicable, and the Manager’s current, reasonable beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund, where applicable, and the Manager believe to be reasonable, neither the Fund, where applicable, or the Manager can assure investors that actual results will be consistent with these forward-looking statements. There is no guarantee that any forward-looking statement will come to pass. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

Neither the Fund, where applicable, nor the Manager assumes any obligation to update or revise any forward-looking statement to reflect new events or circumstances, except as required by law.

The Manager may present the enclosed information in a blog – such blog may contain hypertext links to web sites owned and controlled by parties other than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on such web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.