To download the Auspice February Blog as a PDF, click here.

This month, we are going to talk about a boring yet important topic – inflation and what it implies for portfolio risk and opportunity. Many of the references will be recycled as we have written on this topic for years. Why the redux? Many are calling inflation over, especially in light of the recent US CPI print for January of 2.4% (YoY). However, we believe this print is not only artificially low and not representative of reality (see below) and, more importantly, may be masking implications already showing up in the shape of the interest rate curve.

Economists have suggested the numbers may appear better than reality due to data quirks from the October government shutdown. Moody’s estimates CPI would have been closer to 2.7% had typical data collection occurred.1

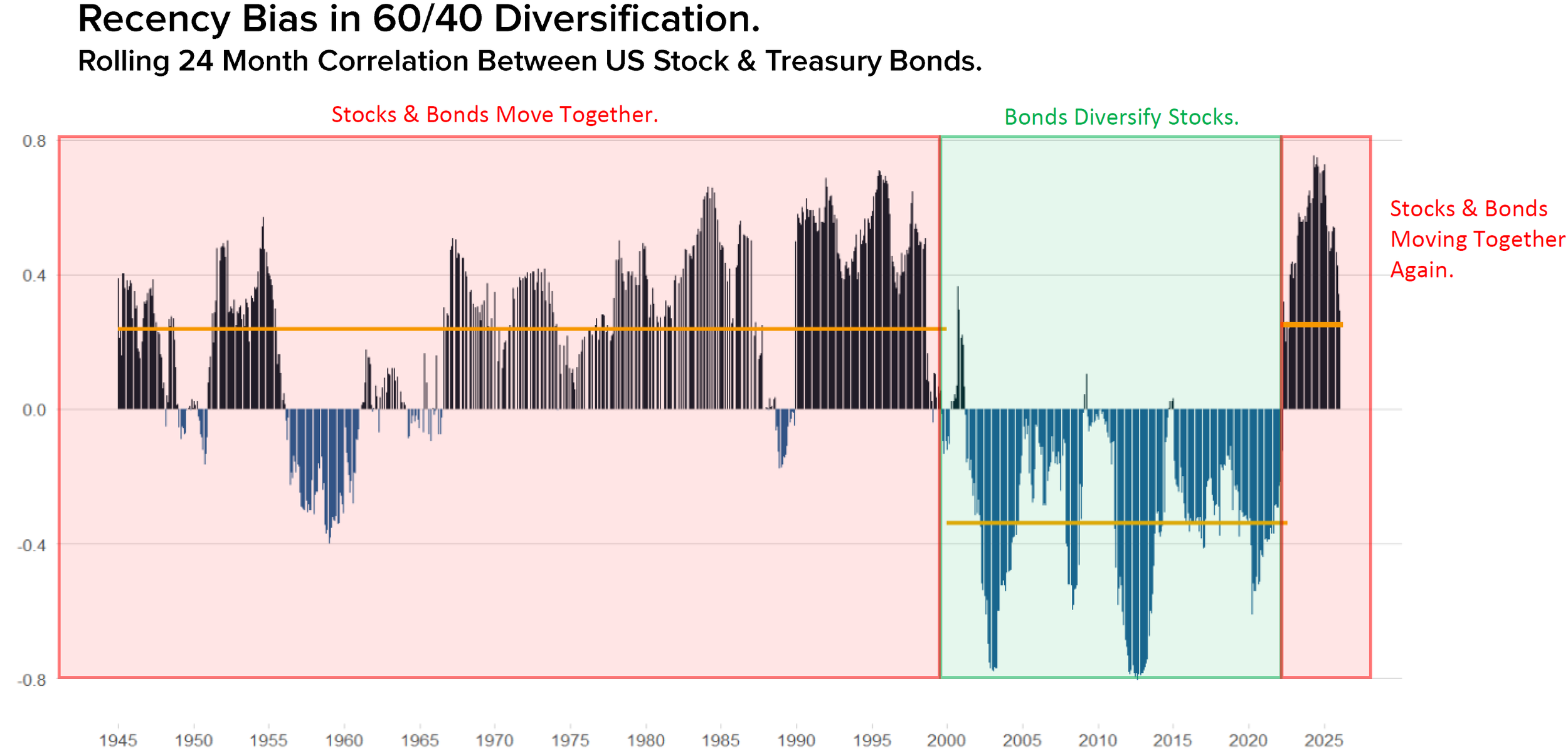

Pre 2000, beyond the tenure of many in the financial business, inflation at some level was normal. In fact, it averaged 3-4% (CPI YoY for last 100 years and since 1970). In this period, per Chart 1, bonds moved in the same direction as equities, not providing the hedge that the next 20+ years did (during a period of almost no inflation). We all got spoiled as the 60/40 portfolio worked. Then 2022 gave us a wakeup call as the so called “60/40 crisis” unfolded. Everything dropped save for commodities, the dawn of what we believe is a new commodity supercycle.

Chart 1: Recency Bias In 60/40 Diversification

Source: Auspice Capital and Global Financial Data as at Dec 31st, 2025. Stocks: S&P 500 Total Return Index, Treasury Bonds: USA 10-year Bond Constant Maturity Yield

Central banks aggressively raised rates to combat inflation which peaked at 9.1% in June 2022. It started to work - until it didn’t. While inflation appears to be moderating it has not changed our view – why? Because while raising rates can help “demand-pull” inflation, it does very little to fight the other type of inflation, “cost-push”. While raising rates indeed helps prevent demand for manufactured goods (consumers spend less as rates go higher), the central banks don’t have the lever for inflation driven by commodities, input costs and wages (cost-push inflation). And that surely hasn’t gone down much.

Proof?

In January, food inflation across the G7 countries averaged 3.5%, with Canada the highest at 7.3%!! This despite roughly 70% of food consumed in Canada being produced domestically.2

Despite inflation moving closer to and even (perhaps artificially) below the 100-year 3% average, we are of the belief that another wave higher is likely coming. The Peterson Institute3 said it well: “We think it is more likely that inflation will surprise to the upside—potentially exceeding 4 percent by the end of 2026. The core drivers are the lagged effects of tariffs, an expansion in the fiscal deficit (which could exceed 7 percent of GDP this year), a tighter labor market reflecting the effects of the shift in immigration policy, monetary policy that is looser than commonly appreciated, and inflationary expectations that are drifting upwards. We believe these factors outweigh the downward-pressure trends that consensus has been fixated on—namely, the ongoing decline in housing inflation and gains in productivity.”

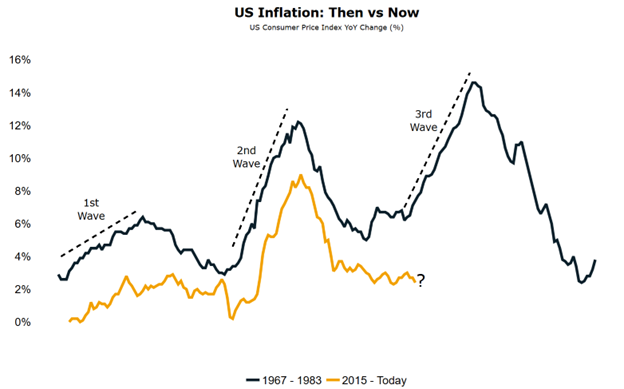

Chart 2 below may depict reality:

Chart 2: US Inflation: Then vs Now (1967-1984 and 2015-Today)

Source: Auspice Capital Operations and Tavi Costa

Regardless of inflation moderating on paper (i.e. CPI), we saw central banks show some of their fears by dropping rates.

Why would they do this?

We first pointed this out last year when it was clear the Trump administration wanted to lower rates in the US (as the UK central bank had just done). Of course, they understand the risk of inflation, but lowering rates helps the economy and moves away from stagflation risk, and per Fed Chair Jerome Powell’s comments on August 22nd, 2025, “this is a distinct possibility”4. In our view, this points toward a growth economy with normal inflation and lower rates, and we should be comfortable with it, as central banks appear to be.

What’s next?

We believe investors need to accept inflation and prepare for it. But beyond the answer of investing in commodities (which we are aware we are bias in saying), investors should consider the shape of the interest rate curve as a clue. We believe that while there may be continued pressure to reduce short term rates to fight stagflation (every politician’s kryptonite), we need a steeper curve. We, along with others, believe 10Y yields may not fully reflect the risks embedded in the system.5 The reality is credit risks are rising and structurally risk isn’t being compensated for. Maybe near term is lower, but time is money and risk.

For example, if inflation wasn’t a risk, it is unlikely the curve would steepen given the downward central bank pressure in the front (short end). Is the current inflation, not mysteriously low numbers, changing the shape of the interest rate curve? We believe yes. Persistent inflation risk, combined with fiscal deficit concerns, is indeed actively changing the shape of the interest rate curve in early 2026, fostering a steepening trend

As of February 2026, the yield curve is transitioning from the deep inversions of 2022 to 2024 toward a more upward-sloping structure. The 10Y–2Y spread has widened as short-term yields decline in anticipation of policy easing, yet long-term yields (10Y – 30Y range) remain elevated, reflecting concern that inflation may persist alongside fiscal deficits. The curve is normalizing in shape, but not necessarily in comfort.6

What’s an Investor to do?

While a steeper curve is generally beneficial for banks, as they typically borrow at lower short-term rates and lend at higher long-term rates, it is a massive risk for investors that use long bonds to hedge inflation risks alongside equity risk. Rates up, bond, price down! Investors should beware of duration risk of the long bonds, which is highly sensitive to inflation shocks.

The "normalization"6 of the curve and ending the inversion signals that the market is beginning to price in a "new normal" for inflation rather than a rapid return to 2010s-style low inflation.

These are indeed conditions where commodities are arguably the best hedge for the following reasons:

Commodities are not correlated to equities

Commodities may be in a long term supercycle after decades of underinvestment and a long list of demand drivers.

Commodities can hedge equity risk especially during times of “normal inflation” where bonds don’t.

Commodities can help reduce duration risk of holding long bonds.

Commodities are the most diverse asset class and trends, both up and down, have accelerated since 2020 and again in 2025-2026.

For investors, this is not about making a short-term call. It is about considering whether commodities deserve a structural allocation within a diversified portfolio when inflation risk is no longer theoretical.

We are again reminded of a quote by Will Rogers over 100 years ago. “Invest in inflation. It is the only thing going up”. While the world is very different, the sentiment should be the same and we believe it is an incredible reminder for investors to beware and use the obvious markets that define inflation itself – commodities.

Footnotes

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results. The views expressed are those of the author and do not constitute investment advice.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus or applicable offering document before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

These materials are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. (the “Manager” or “Auspice”) makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the applicable offering documents before investing.

This material may contain forward-looking statements, which were prepared for the purpose of providing general educational background information and may not be appropriate for other purposes. Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to an Auspice managed investment fund (the “Fund”), where applicable, and the Manager. Forward- looking statements are not purely historical facts but reflect the current expectations of the Fund, where applicable, and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s, where applicable, and the Manager’s current, reasonable beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund, where applicable, and the Manager believe to be reasonable, neither the Fund, where applicable, or the Manager can assure investors that actual results will be consistent with these forward-looking statements. There is no guarantee that any forward-looking statement will come to pass. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

Neither the Fund, where applicable, nor the Manager assumes any obligation to update or revise any forward-looking statement to reflect new events or circumstances, except as required by law.

The Manager may present the enclosed information in a blog – such blog may contain hypertext links to web sites owned and controlled by parties other than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on such web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.