Auspice Managed Futures Excess Return Index (AMFERI)

September Auspice Managed Futures Index Commentary

August Auspice Managed Futures Index Commentary

July Auspice Managed Futures Index Commentary

June Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

The AMFERI has closed the first half of 2013 with a very strong performance gaining 3.09% in June. While much of the global market focus has been on the outperforming Equity sector, the strategy has tactically found opportunity both short and long and across a diverse basket of assets., both commodity and financial. After years of strong gains in Interest Rates (long price, short yield), this sector has gone through transition and has only recently provided opportunity to participate in new trends. While much of the monthly gains have come from being short, the tactical and agile approach employed is proving itself in absolute return and risk management. The strategy is adapting to the market condition and opportunity in an agnostic fashion that continues to provide non-correlated results, specifically when they are needed most.

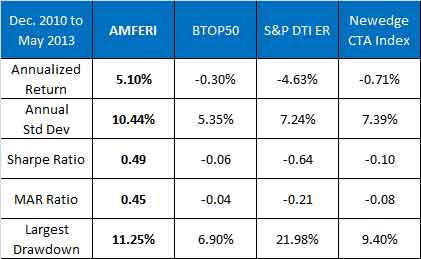

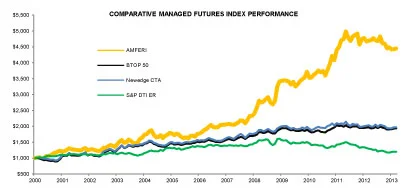

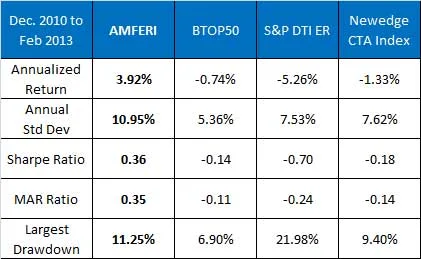

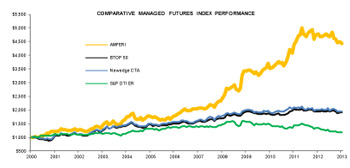

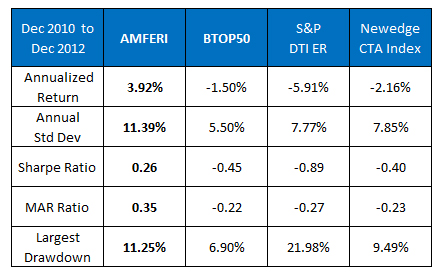

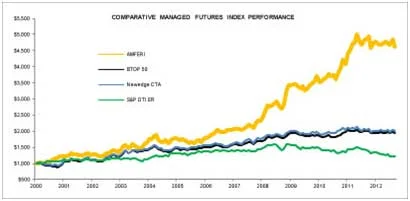

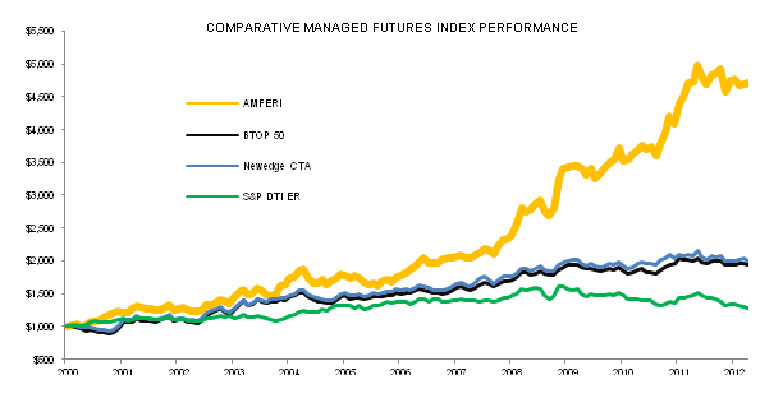

As seen in the next table, the performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

While it is impossible to predict the future, it is important to note that the strong performance by the AMFERI in the first half of 2013 and specifically as the traditional markets correct, is a feature that benefits all portfolios. For it is not just non-correlation, but added performance when you need it most that helps reduce the depth and length of inevitable setbacks in any portfolio.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the below.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

lease contact us at info@auspicecapital.com for the complete analysis.

Index Review

The AMFERI was up 6.01% in Q2 to be up 7.75% in 2013, outperforming a number of investable and non-investable CTA indices.(Highlighted in the table below) As a single strategy CTA index, this strategy provides the benefits of traditional CTA through trend following and agility along with the benefits of transparency and third party publishing, monitoring and benchmarking. The strategy now underlies ETFs, 40 act mutual funds and managed accounts providing a low cost means of allocating to Managed Futures without sacrificing performance.

Portfolio Recap:

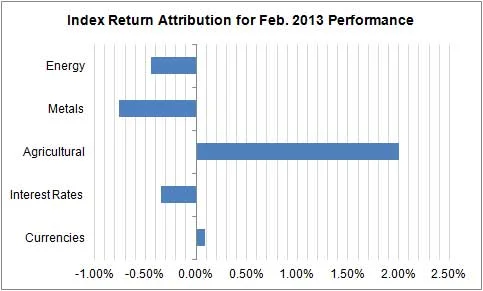

In June the index was up in 4 of the 5 sectors. Gains were made primarily from short positions in both commodities and financial markets. The strongest sector was again Metals. The top performing components within the index were shorts in Gold and Silver complimented by shorts in Wheat, Corn and a long exposure in Cotton. The most challenging sector was Energy. The index is currently positioned short in 9 of 12 commodity markets. The index has further tilted short in the financial markets with 7 of the 9 components holding a short weight. Currencies remain positioned short versus the USD.

Energy

The energy markets corrected against the established trends in Crude and Heating Oil while Gasoline was slightly lower in the direction of trend for a small gain. There were no position changes in Energy as the petroleum weights remain short (Gasoline, Heating Oil and Crude Oil while long Natural Gas). Natural Gas moved sharply lower on the month against the long position. Energy was the most challenging of the sectors for the Index.

Metals

Metals was the strongest performing sector as the index remains short and again benefitted from across the board weakness. The strategy is short weights in Gold, Silver and Copper.

Agriculture

Ags were also large contributors to the strategy gains in June. While the long position in Soybeans was a modest drag, Grains, Wheat and Corn continue to benefit from the trend lower . Meanwhile, a small gain from the long term price deterioration in Sugar and a gain from Cotton also helped the performance from the long side.

Interest Rates

Rates have been challenging in 2013 as the markets gyrate looking for long term direction. The strategy has shifted from long to short a number of times, common during transition in trends while often at the short term expense of return. This choppy price action and position changing has a cost but can be viewed as tactical jockeying while disciplined trend following and risk management is employed. The components have moved back to be tilted short to take advantage of higher interest rates (short bonds) in 2 of the 3 markets as the momentum shifted to lower bond prices. The index switched to short both US 5 year Notes and 30 year long bonds while currently remaining long 10 year Notes.

Currencies

Currencies were modestly profitable despite a choppy and challenging month. Currencies reversed direction a number of times versus the US Dollar and the index benefited from the robust trend filter which avoided trading in and out of the chop. We are holding the same positions: short Aussie dollar in addition to existing shorts in Yen, Canadian dollar, British Pound. The index remains long US Dollar Index and the Euro.

Outlook

The AMFERI has made gains in 2013 alongside the equity market despite the specific lack of equity exposure in the portfolio. In fact there is a negative correlation to the markets despite both being positive on the year. As the equity markets have begun to correct in June, the AMFERI has had a very strong performance with approximately half the volatility of the Equity sector year to date. Consider the non-correlated performance of the index as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Fund Manager/ Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

May Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

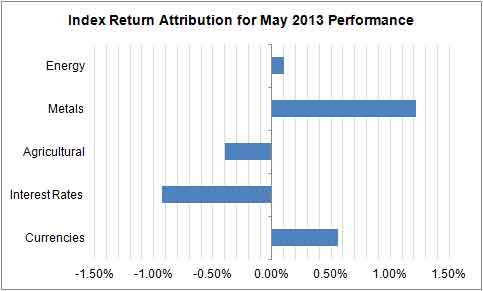

The AMFERI has continued a profitable run in 2013 with a gain of 0.55% in May. This comes despite the market focus on the equity sector which is not part of this single strategy index. While global equity continued its charge higher, interest rates reversed and bond futures fell hard on the month. However, opportunity continued to be found in Metals and Energies as these markets softened. Lastly, the move to USD currency was significant recently and this has been captured within the trend following approach employed in the Auspice index. The portfolio composition and agility is a central feature of the strategy and a number of changes occurred during the month to adapt to ever changing risks and opportunities as highlighted below.

Core allocation: It is important to recognize the value of the managed futures sector is to provide long term absolute return, asset diversification and non-correlation. Given the overall market environment has been very good, especially the performance of the traditional equity and fixed income sectors in the last couple years, managed futures remains an excellent addition to diversify an investment portfolio. The AMFERI is a low cost and transparent ways to get this important exposure

As seen in the next table, the performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

After a period of challenge for many managed futures strategies, the index is off to a strong start in 2013 making back a significant part of the recent modest drawdown. Pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis below.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

Index Review

The AMFERI was up 0.55% in May and is up 4.52% in 2013, outperforming a number of investable and non-investable CTA indices highlighted in the table below. As a single strategy CTA index, this strategy provides the benefits of traditional CTA through trend following and agility along with the benefits of transparency and third party publishing, monitoring and benchmarking.

Portfolio Recap:

In May the index was up in 3 of the 5 sectors. The strongest sector was again Metals. The top performing components within the index were shorts in Gold and Silver complimented by Wheat, Soybeans and Sugar. Gains were made with both long and short positions and both in commodities and financial markets. The most challenging sector was Interest Rates as bonds corrected sharply lower. The index is currently positioned short in 9 of 12 commodity markets reducing one short position. The index is now tilted short in the financial markets with 6 of the 9 components holding a short weight. Within Financials, Currencies are now positioned short versus the USD adding a new short in May. Interest rate components are mixed with a move to short in 2 of the 3 markets as the price trends lower.

Energy

There were no position changes in energy as the petroleum weights remain short (Gasoline, Heating Oil and Crude Oil while long Natural Gas. While Natural Gas moved lower on the month against the position, the rest of the sector was off adding value to the sector for a net gain.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and again benefitted from the significant weakness in Gold and Silver. While the strategy is short Copper which moved higher, this was offset by the gains made. Metals were the most significant attribution to the portfolio gains in May.

Agriculture

With the exception of Cotton, the Ags did very well in May. Led by a short in Wheat, the reversal and new long position in Soybeans were profitable. While Corn rallied modestly against its short, Sugar continued its long term deterioration and the short benefitted. The bulk of the sector loss came from long Cotton which moved significantly lower and will be one to watch closely.

Interest Rates

Rates have been challenging in 2013 as the markets gyrate looking for long term direction. The strategy has shifted from long to short a number of times, common during transition in trends while often at the short term expense of return. This choppy price action and position changing has a cost but can be viewed as tactical jockeying while disciplined trend following and risk management is employed. The components have moved back to be tilted short to take advantage of higher interest rates (short bonds) in 2 of the 3 markets as the momentum shifted to lower bond prices. The index switched to short both US 5 year Notes and 30 year long bonds while currently remaining long 10 year Notes.

Currencies

Currencies were profitable in May as most trended lower against the US Dollar. The index has shifted to short the Aussie dollar in addition to existing shorts in Yen, Canadian dollar, British Pound. The index remains long US Dollar Index and the Euro.

Outlook

The AMFERI is making gains in 2013 alongside the equity market despite the specific lack of equity exposure in the portfolio. In fact there is a negative correlation to the markets despite both being positive on the year. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in May, the ability to generate returns outside of this sole sector should be recognized and considered. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear in traditional asset classes and alternatives. Managed Futures and the AMFERI are a transparent and cost effective way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in May through our shorts in Metals, Energies and Currencies.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Fund Manager/ Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

There were no position changes in energy as the petroleum weights remain short (Gasoline, Heating Oil and Crude Oil while long Natural Gas. While Natural Gas moved lower on the month against the position, the rest of the sector was off adding value to the sector for a net gain.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and again benefitted from the significant weakness in Gold and Silver. While the strategy is short Copper which moved higher, this was offset by the gains made. Metals were the most significant attribution to the portfolio gains in May.

Agriculture

With the exception of Cotton, the Ags did very well in May. Led by a short in Wheat, the reversal and new long position in Soybeans were profitable. While Corn rallied modestly against its short, Sugar continued its long term deterioration and the short benefitted. The bulk of the sector loss came from long Cotton which moved significantly lower and will be one to watch closely.

Interest Rates

Rates have been challenging in 2013 as the markets gyrate looking for long term direction. The strategy has shifted from long to short a number of times, common during transition in trends while often at the short term expense of return. This choppy price action and position changing has a cost but can be viewed as tactical jockeying while disciplined trend following and risk management is employed. The components have moved back to be tilted short to take advantage of higher interest rates (short bonds) in 2 of the 3 markets as the momentum shifted to lower bond prices. The index switched to short both US 5 year Notes and 30 year long bonds while currently remaining long 10 year Notes.

Currencies

Currencies were profitable in May as most trended lower against the US Dollar. The index has shifted to short the Aussie dollar in addition to existing shorts in Yen, Canadian dollar, British Pound. The index remains long US Dollar Index and the Euro.

Outlook

The AMFERI is making gains in 2013 alongside the equity market despite the specific lack of equity exposure in the portfolio. In fact there is a negative correlation to the markets despite both being positive on the year. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in May, the ability to generate returns outside of this sole sector should be recognized and considered. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear in traditional asset classes and alternatives. Managed Futures and the AMFERI are a transparent and cost effective way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in May through our shorts in Metals, Energies and Currencies.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Fund Manager/ Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

April 2013 Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

The AMFERI had a great April as volatility picked up in both financial and commodity sectors alike. While across all global assets, much of the opportunity came from the equity markets, an area not included in this strategy, the index continued to find tactical value in less obvious places. The month was dominated by the Metals market. The portfolio composition and agility is a central feature of the strategy and its intention to provide non-correlation to institutional and retail equity biased portfolios.

As seen in the next table, the performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

After a period of challenge for many managed futures strategies, the index is off to a strong start in 2013 making back a significant part of the recent modest drawdown. Pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the right.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

Index Review

The AMFERI was up 2.27% in April and is up 3.95% (table below) in 2013, outperforming a number of investable and non-investable CTA indices highlighted in the table.

Portfolio Recap:

In April the index was up in 1 of the 5 sectors. The strongest sector was Metal. The top performing components within the index were shorts in Gold, Silver and Copper complimented by Corn, Crude and Sugar. Long gains were made in Natural Gas. The most challenging sector was Ags after having a very strong March on the short side. The index is currently positioned short in 10 of 12 commodity markets and a number of positions changed intra-month. The index is also tilted long in the financial markets with 5 of the 9 components holding a long weight. Within Financials, Currencies remain a balanced short and long (3 and 3). Interest rates components are mixed with a move to long in 2 of the 3 markets as the price trend pushed higher.

In April the index was up in 1 of the 5 sectors. The strongest sector was Metal. The top performing components within the index were shorts in Gold, Silver and Copper complimented by Corn, Crude and Sugar. Long gains were made in Natural Gas. The most challenging sector was Ags after having a very strong March on the short side. The index is currently positioned short in 10 of 12 commodity markets and a number of positions changed intra-month. The index is also tilted long in the financial markets with 5 of the 9 components holding a long weight. Within Financials, Currencies remain a balanced short and long (3 and 3). Interest rates components are mixed with a move to long in 2 of the 3 markets as the price trend pushed higher.

Energy

The petroleum weights have now tilted short – as we have added short positions in Gasoline and Heating Oil while holding short Crude Oil. The index has also moved Natural Gas to a long position for only the second time in 5 years. This was a month of transition for the Energy Sector and the sector was a negative contributor on the month.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and benefitted from the significant weakness in Gold and Silver and to a lesser degree Copper. All metals bounced back at month end but remained sharply lower.

Agriculture

While Ags did very well on the short side in March, most markets corrected in April. Grains moved higher with the exception of Corn and Sugar which continued to drift lower. Cotton remains the lone long position in the sector but was pushed lower for a loss.

Interest Rates

After recently moving all components to take advantage of higher interest rates (short bonds), 2 of the 3 markets have gone long. This is on the back of strong renewed momentum higher in rate futures. The index switched both US 5 year and 10 year Notes to long while remaining short 30 year long bonds. There was a small loss from this sector as positions transitioned on the higher price movement.

Currencies

Currencies were flat in April and position weights remain the same. Small gains were made remaining short the Japanese Yen and long the Euro. Most other markets lacked significant short term trend and we remain positioned with the long term trend. We are long Aussie dollar and US Dollar Index while short the British Pound and the Canadian dollar at this time.

Outlook

The AMFERI was up in Q1 and had a strong start to 2013 alongside the equity market despite a lack of equity exposure in the portfolio. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in April, the sharp sell-off and correction highlight the volatility and risk of the sector. Not all equity markets were up. Many equity markets, including small caps and country specific markets like Canada were lower on the month. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear. Managed Futures and the AMFERI are a good way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in April through our shorts in Metals.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

The petroleum weights have now tilted short – as we have added short positions in Gasoline and Heating Oil while holding short Crude Oil. The index has also moved Natural Gas to a long position for only the second time in 5 years. This was a month of transition for the Energy Sector and the sector was a negative contributor on the month.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and benefitted from the significant weakness in Gold and Silver and to a lesser degree Copper. All metals bounced back at month end but remained sharply lower.

Agriculture

While Ags did very well on the short side in March, most markets corrected in April. Grains moved higher with the exception of Corn and Sugar which continued to drift lower. Cotton remains the lone long position in the sector but was pushed lower for a loss.

Interest Rates

After recently moving all components to take advantage of higher interest rates (short bonds), 2 of the 3 markets have gone long. This is on the back of strong renewed momentum higher in rate futures. The index switched both US 5 year and 10 year Notes to long while remaining short 30 year long bonds. There was a small loss from this sector as positions transitioned on the higher price movement.

Currencies

Currencies were flat in April and position weights remain the same. Small gains were made remaining short the Japanese Yen and long the Euro. Most other markets lacked significant short term trend and we remain positioned with the long term trend. We are long Aussie dollar and US Dollar Index while short the British Pound and the Canadian dollar at this time.

Outlook

The AMFERI was up in Q1 and had a strong start to 2013 alongside the equity market despite a lack of equity exposure in the portfolio. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in April, the sharp sell-off and correction highlight the volatility and risk of the sector. Not all equity markets were up. Many equity markets, including small caps and country specific markets like Canada were lower on the month. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear. Managed Futures and the AMFERI are a good way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in April through our shorts in Metals.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

March 2013 Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

The AMFERI was positive in March while the markets remain dominated by the equity asset class and its sustained move higher. The month March was generally good for trend following and managed futures strategies. As in recent months where the bulk of opportunity came from the equity markets, an area not included in this index, the index continued to find value in less obvious places – predominantly tactical long and shorts in commodities. This agility is a central feature of the strategy and its intention to provide non-correlation to equity biased portfolios.

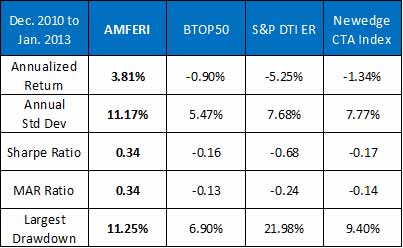

As seen in the next table, the performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

After softening in 2012, the strategy has started to make gains again. Pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the right.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

Index Review

The AMFERI was up 1.01% in March with a quiet month in terms of position changes after a number were made in February. The index was up 1.65% in Q1 (table below), outperforming the investable CTA indices highlighted in the table.

Portfolio Recap:

In March the index was up in 3 of the 5 sectors. The strongest sector was Ags. The top performing components within the index were shorts in Corn, Wheat, Soybeans, and Sugar in addition to a long weight in Cotton. Outside of Ags, long Gasoline was also a strong performer. The most challenging sector was Energies as an aggressive correction higher occurred after the opposite situation in February. Minor gains were also made in the Currency and Metals sectors. The index is currently positioned short in 9 of 12 commodity markets, holding positions since the end of February. The index is also tilted short in the financial markets with 6 of the 9 components holding a short weight. Within Financials, Currencies have a balanced short and long (3 and 3). Interest rates components remain all short.

Energy

The petroleum weights remain the same - long Gasoline and Heating Oil while short Crude Oil and Natural Gas. Unfortunately the long weights did not offset the shorts on the month as Crude and Natural Gas price gains outperformed the long weightings.

Energy has traded strongly higher and lower in the first quarter and March saw a bit of normalization to this behavior. While the index remains short WTI Crude Oil, some of the sector movement higher which was captured by positions in Heating Oil and specifically Gasoline. The sector is currently short Natural Gas which remains on the upper end of a price channel since April 2012.

Metals

The Metals sector is short and benefitted from the significant weakness in Copper and to a lesser degree Silver. Gold was modestly higher offsetting the Copper short for a small sector gain. It is curious that despite the equity market strength and the chatter around economic fundamentals, the reality is the Copper trend remains down.

Agriculture

The Ag sector was the star of the month and highlights the tactical nature of the strategy even within a simingly correlated sector like Ag. Gains were made primarily on the back of short weights (Grains and Sugar) and adding to a solid gain from the lone long position in Cotton which bucked the sector trend and rallied significantly higher.

Interest Rates

The index is now tilted to take advantage of higher interest rates (short bonds). There was a small loss from this sector as prices rose during the month.

Currencies

Currencies made modest sector gains in March. Position weights have not changed since February and thus make the Currency sector evenly balanced long and short. Gains were primarily made on the long side in Aussie dollar and US Dollar Index as those markets moved higher. However, small gains were also made short the Japanese Yen and British Pound. The index remains long the Euro and short the Canadian dollar at this time.

Outlook

The AMFERI was up in Q1 alongside the equity market despite a lack of equity exposure in the portfolio. Consider this fact as one looks for opportunities to reduce risk given the traditional markets have performed well in the last couple of years.

While we don’t know the direction of the traditional equity and fixed income markets, what investors need is an insurance policy that will pay off at times when the inevitable pullbacks occur. In our opinion, AMFERI is better than insurance in that it also has a good chance of making money when you need it the most and at least not losing much, at other times. Overall, your total portfolio has less risk and more chance of making money over the long term by adding a non correlated investment. You wouldn't drive a car without insurance and you shouldn't invest without it either.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

February 2013 Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

While February was generally a challenging month for trend following and managed futures strategies, the AMFERI was positive. As in recent months where the bulk of opportunity came from the equity markets, an area not included in this index, the index found value in less obvious places – shorts in commodities and currencies. This agility is a central feature of the strategy and its intention to provide non-correlation to equity biased portfolios.

The performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

Pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the right.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

Index Review

The AMFERI was up 0.55% in February and was highlighted by a number of position changes further highlighting the period of transition.

Portfolio Recap:

In February the index was up in 2 of the 5 sectors. The strongest sector was Ags followed by Currencies. The top performing component included Corn, Wheat, Crude Oil, British Pound. and the Canadian Dollar – all from the short side. The most challenging sector was in Metals as widespread weakness had the index move from tilted long to short across the sector. Commodities had a positive attribution led primarily by short Ags which outpaced the performance in Metals and Energies both which were down on the back of long positions.

The Currency sector also was positive on the month led by the short in British Pound and the Canadian Dollar. The US Dollar shifted direction and outperformed most global currencies on a move higher.

The index is currently positioned short in 9 of 12 commodity markets, having flipped to short in Gold and Silver in February. The index is tilted short in the financial markets with 6 of the 9 components holding a short weight. Within Financials, Currencies have now balanced short and long (3 and 3) with adding a long weight in the US Dollar Index weight during the month. Interest rates components remain all short.

Energy

The petroleum weights remain the same - long Gasoline and Heating Oil while short Crude Oil and Natural Gas. After a strong January, the petroleum markets sold off aggressively led by Heating Oil and Crude Oil. Natural Gas was slightly higher on the month.

Metals

The Metals sector also moved sharply lower. Both of the remaining long positions in Gold and Silver were moved to shorts. The Copper market also moved lower and benefitted from the sell-off but did not offset the Gold and Silver attribution prior to the shift to short weights.

Agriculture

The Ag sector made great gains primarily on the back of short weights in addition to a small gain from the lone long position in Cotton which moved modestly higher. The Grains, which were tilted short in recent months have continued to correct lower with Wheat the weakest of the three. Sugar remains short as it continues to drift lower. All Ag components, short and long were profitable during February.

Interest Rates

After a big shift in January from a multi-year long position, the index is now tilted to take advantage of higher interest rates (short bonds). There was a small loss from this sector as prices rose during the month.

Currencies

Currencies made modest sector gains in February. Most gains were made on the short side as the US dollar outperformed most markets. The index has now shifted to a long weight in the US Dollar Index. This makes the Currency sector evenly balanced long and short. Currently short British Pound, Canadian Dollar, and the Japanese Yen. Long positions in Euro and Aussie dollar complimented by the new US Dollar Index weight. The Euro and Aussie dollar were both weak but remain long at this time.

Outlook

While we don’t know the direction of the traditional equity and fixed income markets, what investors need is an insurance policy that will pay off at times when the inevitable pullbacks occur. In our opinion, AMFERI is better than insurance in that it also has a good chance of making money when you need it the most and at least not losing much, at other times. Overall, your total portfolio has less risk and more chance of making money over the long term by adding a non correlated investment. You wouldn't drive a car without insurance and you shouldn't invest without it either.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

January 2013 Auspice Managed Futures Index Commentary

Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

January was a mixed month for trend following and managed futures strategies. The AMFERI was slightly positive in a month where the bulk of opportunity came from the equity markets, an area not included in this index. This is a central feature of the strategy and its intention to provide non-correlation to equity biased portfolios.

As such while it appears that market participants are comfortable that the “Fiscal Cliff” has been averted, resulting in an equity rally, the goal of the index remains to follow sustainable trends across multiple assets. Moreover, it is important to point out that while policy and central bank intervention have caused overall choppiness in the diverse global macro sectors represented within the index, this is not always the case.

While the strategy results may slightly lag in moments of times of singular equity sector performance, the opportunity to provide non-correlation and payoff is possible given the strategy's disparate assets and non correlated performance over the long term.

The performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

As previously highlighted, pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the right.

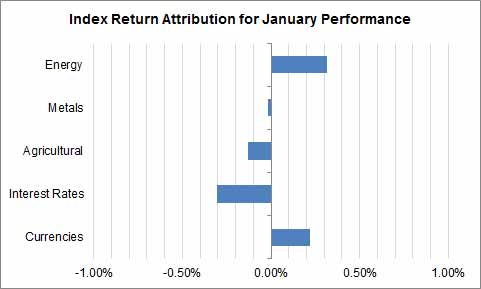

Index Review

The AMFERI was up 0.08% in January and was highlighted by a number of position changes further highlighting the period of transition.

Portfolio Recap:

In January the index was up in 2 of the 5 sectors. The strongest sector was Energy followed by Currencies.

The most challenging sector was in Interest rates as the strategy moved to short Interest Rate futures across the curve (US 5, 10 year Notes and 30 year Bonds). While negative in attribution on the month, this crystallized significant long term gains.

Commodities had a positive attribution led by Energies with Metals and Ags down slightly.

The Currency sector also was positive on the month led by the short in Japanese Yen and Long Euro.

The index is currently positioned long in 5 of 12 commodity markets, having flipped to short in Natural Gas and Soybeans in January. The index is now tilted short in the financial markets with 7 of the 9 components holding a short weight. Within Financials, Currencies have now tilted short adding short British Pound and Canadian Dollar weights during the month. Interest rates components are now all short.

Energy

The weights remain the same - long Gasoline and Heating Oil, short Crude Oil. The petroleum markets are again stronger overall ending January whereas Natural Gas was the outlier and weak.

While the strategy flipped to a long weight in Natural Gas in July 2012 then crystallizing a very profitable short trade, this trend did not extend, As such, the strategy has taken on a new short here.

Metals

The index holds the same long positions in Gold and Silver as ending 2012 while remaining short Copper. The Metals sector has lacked trend commitment for some time although Silver was profitable on the month.

Agriculture

The Ag sector was modestly weaker again led by the Grains. Soybeans were exited during January to now be short the three Grain components. Cotton continued to add value from the long side and was the largest contributor of all components (both financial and commodity). Sugar has continued weak during the month the index remains short for a gain.

Interest Rates

Within this sector, the index is now tilted to take advantage of higher interest rates (short bonds). Long positions had been in place since May 2011 and the bulk of the last 5 years as interest rates fell and have remained low. The sector has been a very profitable weighting for the strategy that has now been crystallized.

Currencies

As in December, Currencies made sector gains in January. The most significant gain came from the short in Japanese Yen complimented by the long Euro weight. Small gains came from long Aussie and short US Dollar Index. The strategy changed to short weight in both the Canadian Dollar and British Pound both which made new lows on the month.

Outlook

Patience: It is important to recognize the value of the managed futures sector is to provide long term absolute return, asset diversification and non-correlation. Given the overall market environment has been very good, especially the performance of the traditional equity and fixed income sectors in the last couple years, Managed Futures remains an excellent addition to diversify an investment portfolio. You wouldn’t drive a car without insurance, and you should remain committed to low cost and transparent ways to get managed futures exposure as well.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

Q4 and 2012 yearly summary AMFERI

Market Review

While it has been a challenging quarter and year in the managed futures sector, the AMFERI has managed to remain low volatility and drawdown relative to its peers and the overall equity market while outperforming many.

As the equity and fixed income markets have performed well in the last few years, the managed futures sector has been challenged by the market environment.

First there are a number of factors that have caused the “risk on” and “risk off” market behavior in 2012: speculation re China growth, the US election, the so called “Fiscal Cliff”, and many others. While each of these things may have contributed to choppy market action (as opposed to volatile and headed in a particular direction), there have been gains made and trends captured. Financial markets have been opportune this quarter and perhaps show a sign that markets are starting to normalize. Now that the “Fiscal Cliff” is behind us, we anticipate the disparate asset classes that provide the unique opportunity in managed futures will yet again show their diversification benefits.

As a result, managed futures remain an important sector to include in a portfolio and this is being recognized by many. In a recent article regarding institutional investors (highlighted on our blog here), it was highlighted that:

- "Year on year, more investors are adding CTAs (managed futures) to their portfolios of alternative asset funds in order to tap into this diversified liquid source of alpha.

- “….more assets have gone to CTAs than any other hedge fund strategies since 2008.”

The performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

As previously highlighted, pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis at below.

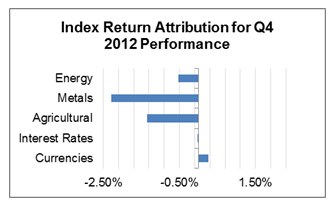

Index Review

The AMFERI was down 1.38% in December for a loss of 3.92% in Q4 and a loss of 7.45% YTD after it gained 8.48% in 2011. The worst drawdown was 8.38%. By comparison the S&P DTI ER was down 11.26% with a worst drawdown of 11.09%. The strategy continues to have a non- correlation to the stock market: +0.12 to S&P500 in 2012, while slightly negative longer term, -0.28 over 5 year highlighting the crisis protection performance.

Portfolio Recap:

In December and throughout Q4, the strongest sectors were the Financials led by Currencies.

The most challenging sectors were in commodities with Metals and Ags providing the bulk of the index softening. The index is currently positioned long in 7 of 12 commodity markets, having flipped to short in Corn and Wheat late in December. The index also remains tilted long in financial markets with 7 of the 9 components holding a long weight. Within Financials, Currencies have now tilted long adding a long Euro weight during the quarter. Interest rates components remain all long.

Energy

After adding Energy commodities steadily in Q3, there were no changes in Q4. The index ended the quarter long Natural Gas, Gasoline, and Heating Oil and short Crude Oil. After lacking direction and overall softer during the quarter, the year ended with the petroleum markets slightly stronger. Natural Gas was the outlier and weak. Watch for changes in weightings early in the New Year as clouds lift from the US election and the “Fiscal Cliff”.

Metals

The index holds the same long positions in Gold and Silver added late in Q3 while remaining short Copper. The Metals sector was soft in Q4 for the majority of the overall index loss with Copper not able to offset the downside in Gold and Silver.

Agriculture

The Ag sector struggled led by the Grains during Q4. The index exited long weightings in Wheat and Corn during the quarter to minimize further downside and participate in the trend lower from the short side. The index remains long Soybeans. The weakest of the Grains was Wheat which after flipping to a short weight actually helped get the Ags to a positive return in December alone. Sugar was weaker during Q4 and the index remains short for a gain while Cotton was modestly stronger and added a long weight early in the quarter.

Interest Rates

The Index remains long Interest Rate futures across the curve (US 5, 10 year Notes and 30 year Bonds) and was near flat performance in Q4.

Currencies

Currencies led sector gains in December and during the quarter. The most significant gain came from the short in Japanese Yen. Other gains came from long British Pound and short US Dollar Index. The sector is now long Aussie, Canadian Dollar, Euro and British Pound while short Yen, Euro and the US Dollar Index.

Outlook

Given the overall market environment, especially the performance of the traditional sectors over the last couple years, Managed Futures remains an excellent addition to diversify an investment portfolio. While the choppy environment and high sector correlation of the last 2 years has been a challenge for the strategy, it is within expectation and should be expected in order to provide the long term benefits of absolute return, asset diversification, and non-correlation. The AMFERI remains an excellent way to get non-correlated performance and crisis protection in a transparent and liquid way.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk.

Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor, pool operator (CTA) and National Futures Association (NFA) member in the US. Auspice’s core expertise is managing risk and designing and executing systematic trading strategies.

Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

AMFERI Market Review Q3 2012

Market Review

The index has shifted to a long stance in the commodity and financial markets since the end of Q2. The index experienced a small loss in September of -0.22% and the quarter -1.68% while the equity markets were very strong. In general, Q3 and the year has been a challenging one for managed futures as the market has been dominated by a few core trends amidst general choppiness and market interventions. The results of the index remain non-correlated relative to traditional asset classes.

Index Review

The AMFERI was down 0.22%% in September for a loss of 1.68% in Q3. The index is down 3.68% YTD after gaining 8.48% in 2011.

Portfolio Recap

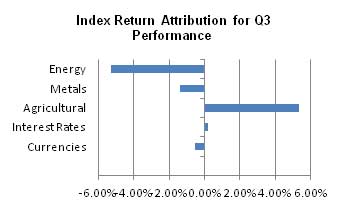

In Q3, the AMFERI index was profitable in 2 of the 5 sectors and negative in 3. The weakest sector within the index was Energy followed by Metals while the strongest was the Agriculture. Interest Rates provided a small gain while Currencies provided a small loss.

The index is currently positioned long in commodities, tilted long in 8 of 12 commodity markets adding 5 new long commodity weights during the quarter. The index is tilted long in financial markets with 7 of the 9 components holding a long weight.

Energy

The Energy sector has shifted from completely short ending Q2 to adding long positions steadily in Q3. First, after experiencing one of the longest downtrends in the commodity history, Natural Gas went long in July. Gasoline followed in August and Heating Oil went long in September. The index is currently short Crude Oil position and this market was the weakest of the sector during September.

Metals

After leaving Q2 short, the index has shifted to long positions in Gold and Silver during September. The index is still short Copper at this time but this will be one to watch.

Agriculture

The Ag sector led the index with gains provided by the Grains during Q3. Each of the Grains added value and remain with long weightings at this time (Corn, Wheat, Soybeans). Most of the gain was made early in the quarter. Sugar was weaker during Q3 and contributed to the sector performance from the short side while Cotton was modestly stronger for a small loss.

Interest Rates

The Index remains long Interest Rate futures across the curve (US 5,10 year Notes and 30 year Bonds). This sector was profitable in Q3.

Currencies

Currencies provided a small loss in Q3 as many of these markets changed position during the quarter and were generally choppy and in transition. The index moved from short to long in the Aussie and Canadian Dollars as well as the Japanese Yen. Significant gains were again made from the long weight in British Pound while the Euro short was not profitable but held. Lastly, the index moved to a short in the US Dollar index as the Dollar showed weakness through the latter half of the quarter.

Outlook

Managed Futures remains an excellent place to be given the current market volatility and risk. While the recent performance has been slightly negative, the correlation to traditional markets remains low. The AMFERI remains an excellent defensive place to get non-correlated performance and crisis protection.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk.

Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor, pool operator (CTA/CPO) and National Futures Association (NFA) member in the US. Auspice’s core expertise is managing risk and designing and executing systematic trading strategies.

Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

AMFERI Market Review Q2 2012

Market Review

While many commonly suggest that CTAs have trouble in periods without trend, we recognize that this is a challenge for most strategies and not a very good explanation. Throughout Q2 and much of 2012, the market has been highlighted by choppy volatility, central bank interventions, and sharp reversals which are indeed difficult times for most managed futures strategies. In these periods it is often a good result to gain sideways performance and modest pullbacks which are a reality and trade-off in producing non-correlated performance.

Since equity markets moved lower starting in March/April and continued sharply lower in May, the diversification benefits of Managed Futures added value and a measure of reassurance in an otherwise volatile environment. While a negative period of performance does not feel good, it needs to be taken in the context of the overall portfolio and the gains made across all assets. If you consider the market still at risk and/or are looking for non-correlated diversification, this may be an entry point to consider.

Index Review

The AMFERI was down 0.55% during Q2 and is -1.90% YTD after gaining 8.48% in 2011. By comparison, the S&P DTI (Diversified Trends Indicator Price Return) lost 6.24% during the quarter and -10.24% YTD.

Portfolio Recap:

In Q2, the AMFERI index was profitable in 2 of the 4 sectors, negative in 2 and flat in 1. The weakest sector within the index was Energy which started to soften significantly at the end of Q2. Currencies also remained a challenge. Sector gains were made in Agricultures led by weakness in Softs and long Interest Rates. Metals were flat on the quarter.

The index is currently positioned defensively, tilted short in 9 of 12 commodity markets, protecting from downside in many commodities. It is also short 4 of the 9 financial markets all within the currency sector. Interest rates remain long. In total 13 of 21 markets are short.

Energy

While the index added long positions in Crude Oil, Heating Oil and Gasoline in Q4 2011 and early in 2012 which provided gains in Q1, the market softened dramatically in Q2. The index has reversed and gone short in all 3 of those markets. The index remains short Natural Gas since July 2008 despite some of the recent gains. Natural gas has remained in a downtrend since mid 2008. This sector was not profitable in Q2 providing the bulk of the index loss.

Metals

The Metals sector is positioned short. The index was long Silver much of Q2 but has now reversed to be short near the end of June. Copper and Gold continue to trend lower remain a short weight. This sector was not profitable in Q2.

Agriculture

The Ag sector provided gains led by the weakness in Soft Commodities during Q2. Cotton, which was shorted midway through 2011 continued to experience weakness in Q2. Sugar was also weaker during Q2 and was a profitable short exposure. While each of the Grains acted in a unique manner and is treated discretely, all have long weightings at the end of Q2. Soybeans remain long since Q1 while Corn and Wheat flipped from short to long during the quarter. Corn was added at the end of June while Wheat was added at the end of May. Grains were flat on the quarter.

Interest Rates

We remain long interest rate futures across the curve (US 5 and 10 year Notes and 30 year Bonds) although movement higher was modest. This sector was profitable in Q2.

Currencies

Currencies remain very choppy highlighted by short term trend reversals inspired by central bank and policy interventions. While the strategy was profitable holding a short in the Euro and long the US Dollar Index, the other currencies were a challenge. In May, the Aussie and Canadian dollar which had been long and in uptrend reversed and headed lower. The strategy went short Aussie in May and short Canadian dollar in early June. The long British Pound also pulled back heavily where the index remains long. Lastly, our short in Japanese Yen rallied against the trend and moved higher. As such, it was a challenge in currencies but we have made some adjustments.

Outlook

Managed Futures remains an excellent place to be given the market volatility and risk. Adding non-correlation and crisis alpha during this time is a responsible thing to do. The strategy remains non-correlated despite short term periods of challenge.

September Commentary & Performance

September was a choppy month as we experienced extended weakness and increased volatility across many asset classes. While our performance was negative on the month - the quarterly, year to date, and long term results continue to illustrate the non-correlated benefits of managed futures. Moreover, we continue to provide "event" protection as we experienced in 2008 and so many other times in history.

As measured by the S&P 500, the equity markets experienced one of the worst quarterly performances in history, down over 14%. While managed futures did not provide a perfect offset, the strategy did perform much better -1.52%. This brings up two benefits to adding Managed Futures to a portfolio:

First, Managed futures provides non-correlation to the broad markets, not necessarily negative correlation. If equity markets decline it does not mean that managed futures will be positive. Managed futures have little or no relationship with the returns of the equity markets, although sometimes they do move in the same direction.

Measuring correlations over short periods of time is less valuable as a statistic. Ideally this is measured over a period of years that encompasses many market environments and situations. Over the long term, our correlation to the S&P is -0.26. It is a non-correlated number that is slightly negative that highlights the benefits that have been achieved during periods of financial stress.

Second, another goal of managed futures is to provide a benefit during times of significant financial stress, what some describe as "Tail Risks". During this quarter, Auspice Diversified did just that. If the past is any indication, prolonged weakness could be harnessed very well by the Auspice strategy as the event unfolds and tail risk protection is needed.

- Q3 2008: -1.15%

- Q4 2008: +20.40%

- Q3 2011: -1.52%

- Q4 2011: ???

Click here for an excellent article on Tail Risk protection.

Take comfort in your investment at Auspice and our disciplined approach to the markets. Auspice practices an active risk management and capital allocation model. Thus, we adjust our exposure based on market risk. As with previous times in history, Auspice has actively adjusted risk to remain within our targeted level based on market volatility, liquidity and mark to market gains in the portfolio. All of these things ensure we will continue to crystallize opportunities while remaining appropriately involved in the markets during these opportune yet volatile times.

Highlights of the month: In September, the Auspice Diversified Program was profitable in 3 of the 7 sectors traded. The profitable sectors included Interest Rates, Equity Indices and Energies. Of the unprofitable sectors, many of them broke their uptrends or turned down substantially on the month.

Since full diversification (achieved in June 2007) the annualized return is now +11.2% with 13.5% volatility or 25-30% lower volatility than the Equity market. The global equity markets remain negative over this same period.

Interesting trades: During the month, we took profits in the other commodity currency, the Aussie dollar, which had been held since July 2010. We also took profits in US 2 year Notes, a long trade entered in May 2011. Lastly, we took profits in a long Orange Juice trade that was initiated in September 2010.

Key Points Regarding our Positions

Energies: The Energy markets were weak across the board in September. We remain short Crude Oil and Natural Gas, both which continued to trend lower. We remain on the sidelines in Heating Oil and Gasoline but are monitoring closely for further signs of deterioration.

Metals: We remain long Gold despite recent weakness as the long term trend remains intact. We entered a new short in Palladium as this market broke down from long term trading ranges helping to affirm the trend lower. We remain on the sideline in Copper at month end but have noted that it is no longer in an uptrend by our definition. The Gold market is the strongest of the sector as it has been for many months. Overall this sector was not profitable on the month.