To download the Auspice May Blog as a PDF, click here.

This commentary is intended for general informational purposes only and does not constitute investment advice or a recommendation.

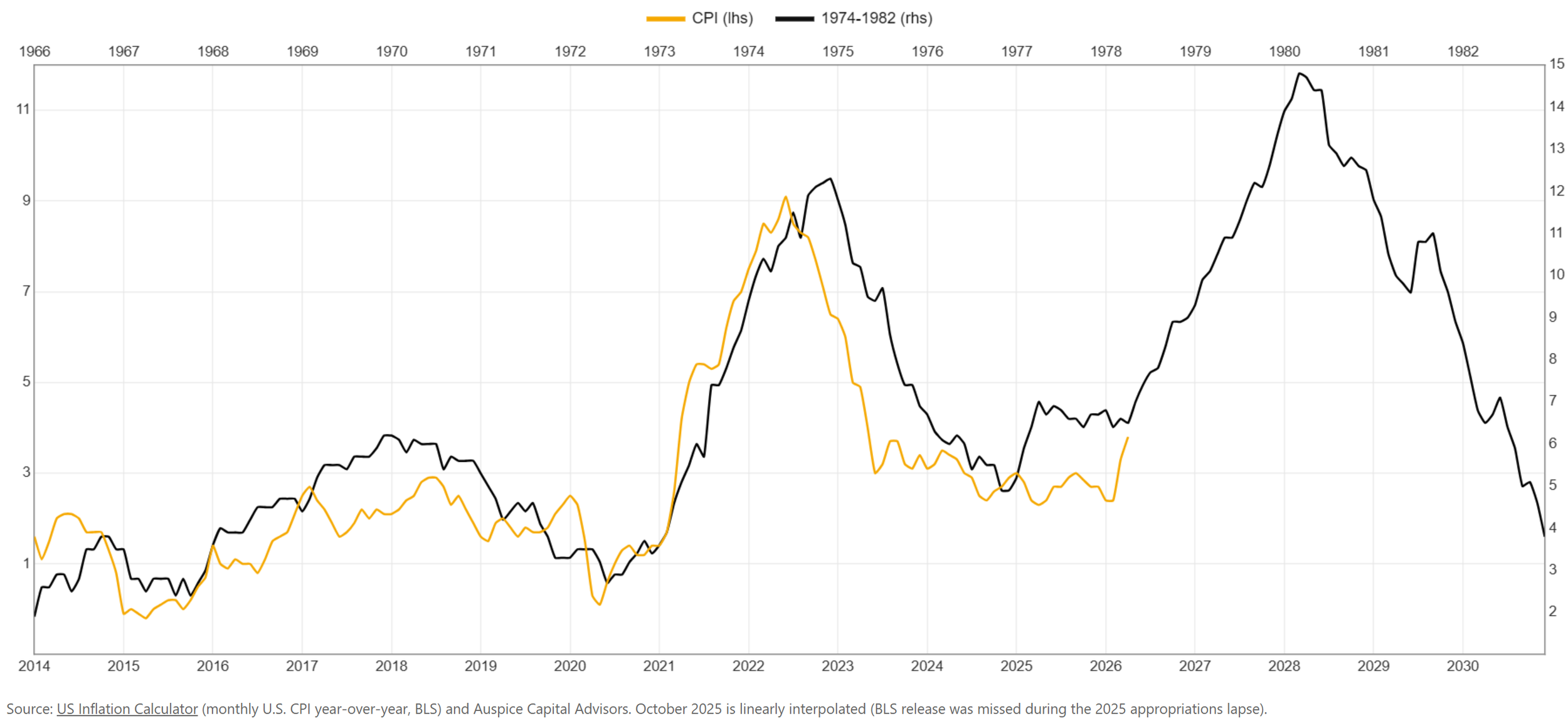

The similarities are uncanny: the sideways inflation from 2014 into 2020 is like a mirror to 1966 into 1972. Then the rally and moderation followed by another phase, as shown in Chart 1.

Chart 1: Current versus 1970 Inflation Cycle

Of course, we acknowledge the differences; the world has changed and history does not have to repeat. However, everything is suggesting to us that it could be very similar in terms of a commodity and wage-driven, cost-push inflation-driven cycle.

Why?

Another Conflict

The US-Israel-Iran conflict is obvious, but how its effects materialize isn’t as explicit.

In the US and Western world in general, it is showing up as actual household inflation from food, energy prices and transportation costs (gasoline/diesel).

However, in China, where goods are manufactured, the price shock out of the Strait of Hormuz is more upstream. Think the price of making the goods that the rest of the world consumes. This includes the same price of fuel, which translates to freight costs, but also the raw materials needed to make the goods.

This includes a range of metals, chemicals, gases (helium) and the inputs to make things. Per permutable.ai, China’s PPI has broken out of a deflation cycle that began in late 2022, rising from -0.9% YoY in February to 2.8% YoY in April, a 45-month high. Meanwhile, in the US, April CPI accelerated to 3.8% YoY, up from 3.3% in March, with energy accounting for more than 40% of the monthly increase.1

Both in the US and China, there exists intense inflationary pressure. It is manifesting in different, but equally significant, ways (See Figure 1).

Figure 1: US CPI vs China PPI April 2026

Importantly, one could argue, it is the exact WRONG kind of inflation for central banks. Reminder: central banks have tools to deal with demand-pull inflation, demand for manufactured goods. They do not have great tools for cost-push inflation. This is a different animal yet the same beast as the 1970's.

AI and Electrification – What’s the play?

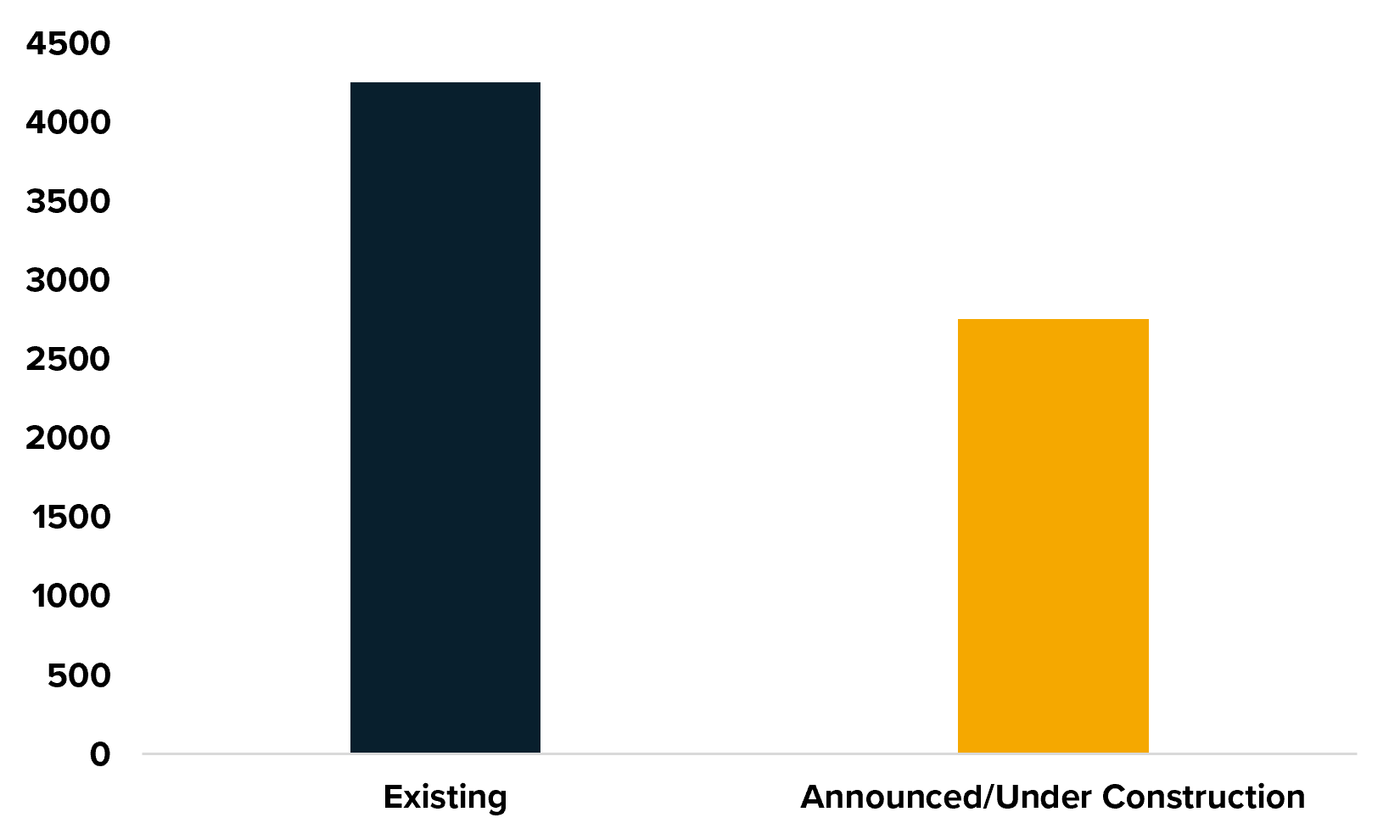

While upcoming massive IPOs in AI are taking up headlines, we believe the real trade is brick and mortar. According to Apollo, America's data center count is about to nearly double.2 From nearly 4,000 existing data centers, there are almost 3,000 data centers that are announced / under construction (See Chart 3).

Chart 2: Existing and Announced/Under Construction Data Centers

Source: Data Center Map - Database

So at a time when household inflation is climbing because of commodity prices, and input costs to make things are rising, the biggest companies in the world are fighting a commodity war to build. Not just the chips, the infrastructure - and it eats commodities.

So what is an investor to do?

"Given that inflation is heading in the wrong direction and the labour market is holding up, it's very unlikely that the Fed will be able to lower interest rates any time soon," said Chris Zaccarelli, chief investment officer at Northlight Asset Management, in a report by CNBC. Rates continue to rise, and thus bonds fall. They are not the hedge we hoped for.

The hedge? Commodities.

Last month, we said what we had wrong. The commodity cycle wasn't 10 years from 2020, but rather it reset and is likely 10+ years from 2025. Just days ago, this was reiterated by Jeff Currie of the Carlyle Group and Goldman Sachs' former Head of Commodities Research. "The world is in the early stages of a commodity supercycle that may last another decade or more as the artificial intelligence buildout collides with chronic underinvestment in energy and materials capacity... the supercycle could run 10 to 12 more years."

SOURCES

https://permutable.ai/china-inflation-2026-ppi-45-month-high/

https://www.apollo.com/wealth/the-daily-spark/americas-data-center-count-is-already-near-double

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results. The views expressed are those of the author and do not constitute investment advice.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus or applicable offering document before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

All data is believed to be reliable but has not been independently verified.

The indices shown (Charts 1-5) are for illustrative purposes only. Index returns do not reflect the deduction of fees, expenses or transaction costs. Past performance is not indicative of future results. The referenced indices are not directly investable. Also, where ETF or index proxies are used, they are intended to approximate the performance of the underlying strategy and may not reflect actual investable results.

These materials are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. (the “Manager” or “Auspice”) makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the applicable offering documents before investing.

This material may contain forward-looking statements, which were prepared for the purpose of providing general educational background information and may not be appropriate for other purposes. Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to an Auspice managed investment fund (the “Fund”), where applicable, and the Manager. Forward- looking statements are not purely historical facts but reflect the current expectations of the Fund, where applicable, and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s, where applicable, and the Manager’s current, reasonable beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund, where applicable, and the Manager believe to be reasonable, neither the Fund, where applicable, or the Manager can assure investors that actual results will be consistent with these forward-looking statements. There is no guarantee that any forward-looking statement will come to pass. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

Neither the Fund, where applicable, nor the Manager assumes any obligation to update or revise any forward-looking statement to reflect new events or circumstances, except as required by law.

The Manager may present the enclosed information in a blog – such blog may contain hypertext links to web sites owned and controlled by parties other than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on such web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.