As investors we tend to look to the past to infer the future. For the last decade and a half, equity selloffs have generally been brief, and portfolios have been buoyed by strong performance in bonds which in turn were buoyed by unprecedented quantitative easing.

Even longer term, in multi-year equity bear markets (remember those?) portfolios have been cushioned by strong performance in bonds. It hasn’t been the decade of the 60/40 portfolio – it has been the generation.

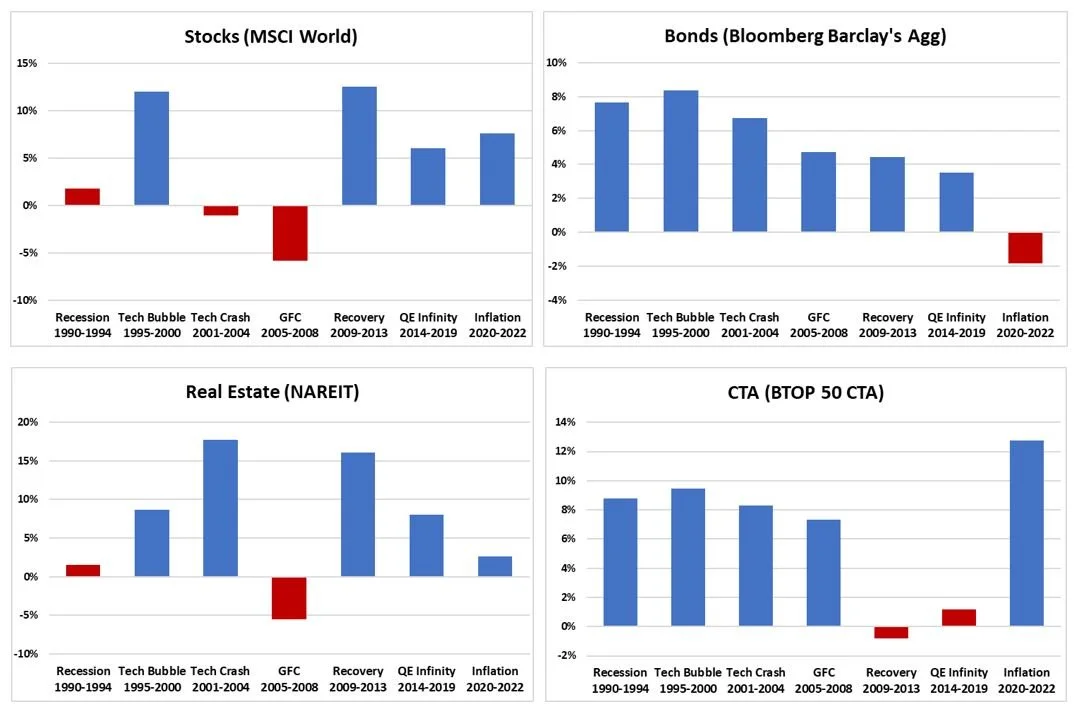

For retail investors in particular it has been a tremendous, unprecedented period of returns. Not only has the 60/40 portfolio thrived, but so too has real estate. If we look at various regimes, or themes that characterized 3-5 year periods, the current inflationary regime that began in 2020 marks the first departure from consistent stock/bonds/real estate returns since the Global Financial Crisis (GFC).

Source: Auspice & Bloomberg. 2022 data through April 29th, 2022.

And while the traditional portfolio previously thrived, it was an unprecedent period of challenging returns for Commodity Trading Advisors (CTAs). Previously CTAs, alongside providing “crisis alpha” and inflation protection, were also sought for returns enhancement – from 1987 to 2010 the benchmark BTOP 50 CTA Index annualized a +9.2% return, outperforming most stock and bond indexes (we will be sharing more on CTAs specifically in an upcoming May AIMA partnered publication “The Resurgence of Trend Following”).

What the bond market is telling us.

When we think of the past we struggle to think beyond our most recent experiences. We are all aware of recency-bias and shortermism, but the reality is that these biases have led to exceptional investment returns, and they can be challenging to overcome. “Buying the dip” and rebalancing stock/bond portfolios has been simple and effective - this mentality has been consistently reinforced and rewarded last decade.

But 2020 might not just have marked a new short-term regime or cycle, but a potentially new multi-decade secular cycle in which stocks, bonds, and real estate are not buoyed by quantitative easing and declining interest rates. 2022 is already highlighting how extraordinarily different today’s environment is for bond investors. As per Jim Bianco:

“Carnage. The Bond market, proxied by the Bloomberg Global Aggregate Index ($68 trillion in AUM and more than 28K bonds) has lost more than 10% YTD. Never happened before. A classic example of a Black Swan event”.

Source: Bianco Research on Twitter

This bond selloff – coinciding with an equity selloff, particularly pronounced in technology and growth stocks, is catching many investors off guard. For millennials and younger investors, it’s unprecedented. Not only are declines significant in their magnitude, but also in their duration – previous equity and bond selloffs have been met with sharp rebounds. There has been little to rebalance to/from in the traditional portfolio, and buying the dip, often through margin, could prove dire.

Investors need to look beyond the most recent 10-15 years for cues to position their portfolios going forward. The environment most investors have grown accustomed to – characterized by declining interest rates alongside artificially low inflation and volatility – has likely ended.

Disclaimer below

IMPORTANT DISCLAIMERS AND NOTES

1. The MSCI World Index, Morgan Stanley Capital International, is designed to measure equity market performance large and mid-cap equity performance across 23 developed markets countries, covering approximately 85% of the free float-adjusted market capitalization in each. This index offers a broad global equity benchmark, without emerging markets exposure.

2. The Bloomberg Barclay’s Aggregate Bond Index, or the Agg, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. Investors frequently use the index as a stand-in for measuring the performance of the US bond market.

3. The FTSE EPRA/NAREIT Global Real Estate Index is a free-float adjusted, market capitalization-weighted index designed to track the performance of listed real estate companies in both developed and emerging countries worldwide. Constituents of the Index are screened on liquidity, size and revenue.

4. The Barclay BTOP50 CTA Index seeks to replicate the overall composition of the managed futures industry with regard to trading style and overall market exposure. The BTOP50 employs a top-down approach in selecting its constituents. The largest investable trading advisor programs, as measured by assets under management, are selected for inclusion in the BTOP50.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise.

QUALIFIED INVESTORS

For U.S. investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, is only available to Qualified Eligible Persons “QEP’s” as defined by CFTC Regulation 4.7.

For Canadian investors, any reference to the Auspice Diversified Strategy or Program, “ADP”, or Auspice One Fund “AOF”, is only available to “Accredited Investors” as defined by CSA NI 45-106.