To download the Auspice November Blog as a PDF, click here.

This communication discusses indices and may reference model or hypothetical performance for illustration. It reflects Auspice thought leadership and is provided for informational purposes only. Please see the Important Disclaimers and Notes section below for full details.

Undoubtedly, one of the top-performing asset classes over the first five years of this decade has been equities, particularly the de facto benchmark – the S&P 500. It is hard to argue with 13% annualized, albeit this came with significant volatility, a 25% drawdown, and negative skew (downside moves and volatility are greater than the upside). But what alternative assets could be added to improve the client experience and ultimately portfolio outcomes – less volatility, less drawdown, less downside volatility, and higher Sharpe? Alternatives are not created equally. Their underlying risk factors, liquidity constraints, capital efficiency, and sources of yield differ widely - meaning some “alts” truly diversify while others repackage economic growth exposure.

Alternatives are Not All the Same

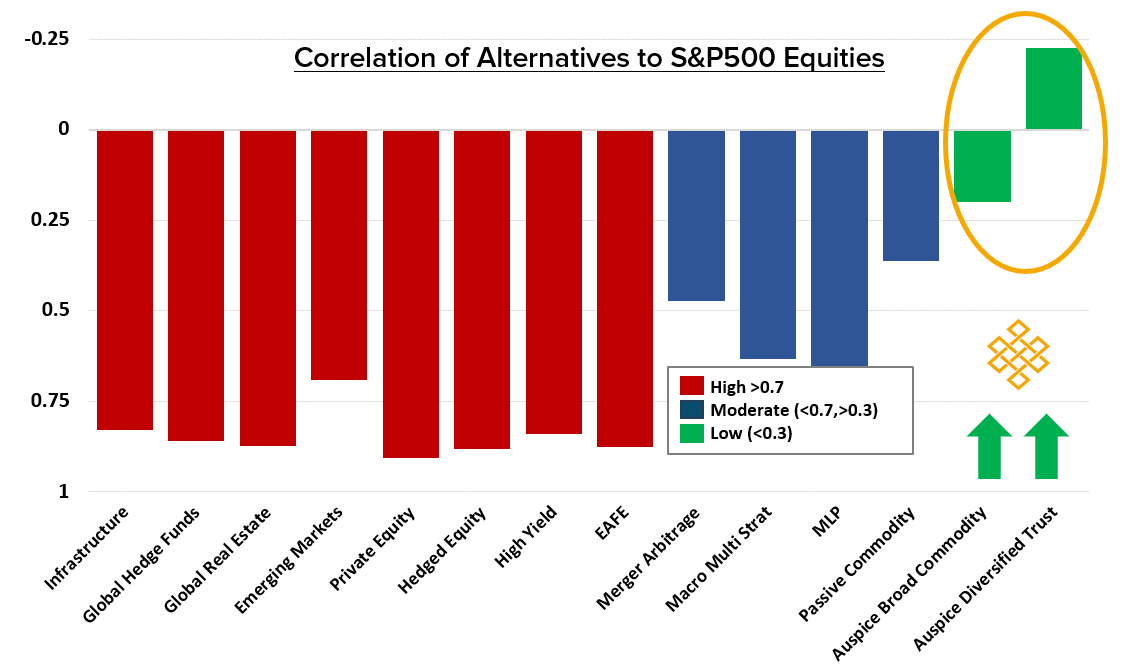

We have long shown that many of the widely used “alternatives” have a materially high correlation, over 80%, to equity beta (S&P 500), as visible in red in Chart 1. Although they may appear attractive for a number of reasons, their accretive value from a portfolio lens is actually less than that of those with a low to negative correlation. This remains true even when the high-correlation alternative has a higher stand-alone return than the diversifier. Furthermore, if the negatively correlated alternative can be layered on top of the core portfolio, the addition may improve portfolio diversification without altering the core holdings.

Chart 1 – Alternatives Not All the Same:

To illustrate this, we will begin by reviewing the stand-alone performance of the S&P 500, the Bloomberg All Hedge Fund Index (BHEDGE), and Auspice Diversified Trust (ADT). We then add a 20% BHEDGE allocation to an S&P 500 portfolio and evaluate how the resulting portfolio metrics compare to substituting the same 20% allocation into ADT.

Stand-alone Performance

Per Table 1, since 2020, BHEDGE has a higher return than ADT, but also a notably high correlation to the S&P 500 at 0.86 relative to ADT’s -0.18.

Table 1: Stand-alone Performance

| Index (Jan 2020 – Oct 2025) |

Ann. Return |

Cum. Return |

Sharpe | Max Drawdown |

Volatility | Skew | S&P 500 Correlation |

|---|---|---|---|---|---|---|---|

| S&P 500 | 13.73% | 111.72% | 0.86 | -24.77% | 17.37% | -0.42 | 1.00 |

| BHEDGE | 7.03% | 48.63% | 1.01 | -10.95% | 7.13% | -1.17 | 0.86 |

| ADT | 5.36% | 35.59% | 0.55 | -18.60% | 10.39% | 0.96 | -0.18 |

Alternative Addition to Equity Beta

First, we consider the 20% allocation to BHEDGE. The result in Table 2 below shows that, given the lower annualized return relative to the S&P 500, the combined return drops modestly to 12.47% annualized. However, the risk metrics show an increase in Sharpe, largely thanks to 13% lower relative volatility and a 12% lower relative drawdown. We see the consequences of increased factor exposure in the skew metrics. Equity and similar high correlation return streams tend to drift up but have outsized downward moves; this is also described as a convergent return stream. These return streams tend to feel reassuring because they are frequently positive; even small green numbers are perceived as progress, whereas equally small red numbers trigger loss aversion. But that behavioral comfort comes at the cost of the distinct risk-mitigating benefits investors typically seek in alternatives.

Table 2: S&P 500 vs 80% S&P 500 20% BHEDGE

| Index (Jan 2020 – Oct 2025) |

Ann. Ret |

Cum. Ret |

Sharpe | Max Drawdown |

Volatility | Skew |

|---|---|---|---|---|---|---|

| S&P 500 | 13.73% | 111.72% | 0.86 | -24.77% | 17.37% | -0.42 |

| 80% S&P 500 / 20% BHEDGE | 12.47% | 98.41% | 0.89 | -21.75% | 15.15% | -0.47 |

| Change Analysis | -9.20% | -11.90% | +2.70% | -12.20% | -12.80% | -12.00% |

Now we look at the negatively correlated alternative in ADT. The result in Table 3 shows that, regardless of ADT’s lower annualized return relative to both the S&P 500 and BHEDGE, its addition has a slightly smaller impact on reducing the portfolio’s overall annualized return. Moreover, when considering the risk metrics, we now see material enhancements in Sharpe with a more than 20% decrease in volatility and a 30% decrease in drawdown. A key difference in the comparison comes from this alternative's characteristic of positive skew (upside moves and volatility are greater than the downside). This helps smooth the convergent equity stream, resulting in both a better client experience and a stronger portfolio outcome despite the lower stand-alone return. These benefits arise only when the portfolio incorporates a genuinely differentiated factor, asset class or risk driver - not simply another form of economic-growth risk with a different label.

Table 3: S&P 500 vs 80% S&P 500 20% ADT

| Index (Jan 2020 – Oct 2025) |

Ann. Ret |

Cum. Ret |

Sharpe | Max Drawdown |

Volatility | Skew |

|---|---|---|---|---|---|---|

| S&P 500 | 13.73% | 111.72% | 0.86 | -24.77% | 17.37% | -0.42 |

| 80% S&P 500 / 20% ADT | 12.53% | 99.06% | 0.97 | -17.31% | 13.67% | -0.31 |

| Change Analysis | -8.70% | -11.30% | +12.30% | -30.10% | -21.30% | +26.00% |

Beyond Equities

Looking beyond equities, we now move to the portfolio level. Using a simple hypothetical 60/40 mix of the S&P 500 and the Bloomberg U.S. Agg Total Return Index (LBUSTRUU), we then extend it to a 50/30/20 portfolio that incorporates alternatives and measure the impact on overall portfolio outcomes.

Considering BHEDGE, the result shown in Table 4 highlights a similar slight lowering of the annualized return by a mere 7bps. We can also see similar small improvements across the risk metrics as with the equity-only portfolio, with 6% higher Sharpe, 7% lower volatility, and a 10% lower drawdown. Unfortunately, as before, the skew becomes even more negative for the combination as highlighted.

Table 4: 60/40 vs 50/30/20 BHEDGE

| Portfolio (Jan 2020 – Oct 2025) |

Ann. Ret |

Cum. Ret |

Sharpe | Max Drawdown |

Volatility | Skew |

|---|---|---|---|---|---|---|

| 60% S&P 500 / 40% LBUSTRUU | 8.81% | 63.65% | 0.80 | -20.69% | 11.86% | -0.39 |

| 50% / 30% / 20% BHEDGE | 8.74% | 63.01% | 0.85 | -18.64% | 10.98% | -0.45 |

| Change Analysis | -0.80% | -1.00% | +5.90% | -9.90% | -7.40% | -14.50% |

Table 5 again shows that despite the lower stand-alone return, the addition of the negatively correlated alternative asset in ADT results in a nearly identical return at 8.69% - a reduction of only 12bps. However, we now observe a material positive change in risk metrics following the BHEDGE addition, with a 19% higher Sharpe, a 20% lower relative volatility, and a 32% lower drawdown. The additional upside volatility also appears at the portfolio level, decreasing the negative skew for the combination by over 22%.

Table 5: 60/40 vs 50/30/20 ADT

| Portfolio (Jan 2020 – Oct 2025) |

Ann. Ret |

Cum. Ret |

Sharpe | Max Drawdown |

Volatility | Skew |

|---|---|---|---|---|---|---|

| 60% S&P 500 / 40% LBUSTRUU | 8.81% | 63.65% | 0.80 | -20.69% | 11.86% | -0.39 |

| 50% / 30% / 20% ADT | 8.69% | 62.55% | 0.96 | -14.04% | 9.54% | -0.31 |

| Change Analysis | -1.40% | -1.70% | +18.90% | -31.90% | -19.60% | +22.60% |

Structural Advantages

What if the 20% alternative allocation didn’t need to replace part of the 60/40, and could instead sit on top of it, as shown in Figure 1? CTA strategies like Auspice Diversified Trust make this possible because they require very little capital to access their exposures. This is the premise behind the return-stacking design of the Auspice One Fund Trust (AOFT): by swapping an existing S&P 500 position for AOFT, investors keep their equity exposure and gain the diversifier on top. This is achieved by selling 20% S&P 500 exposure and obtaining the exposure within AOFT alongside a 20% allocation to the ADT diversifier. Note: While this structure involves the use of derivatives and the possibility that realized exposures may differ from intended allocations, the same is true for most exposures to the S&P 500 through ETFs using swaps and futures

Figure 1: Return Stacking Construction

As Table 6 shows, by adding ADT on top while maintaining the original core exposures, we can add real value.

| Portfolio (Jan 2020 – Oct 2025) |

Ann. Ret |

Cum. Ret |

Sharpe | Max Drawdown |

Volatility | Skew |

|---|---|---|---|---|---|---|

| 60% S&P 500 / 40% LBUSTRUU | 8.81% | 63.65% | 0.80 | -20.69% | 11.86% | -0.39 |

| 60% / 40% / 20% ADT | 10.15% | 75.69% | 0.93 | -17.88% | 11.59% | -0.33 |

| Change Analysis | +15.10% | +18.90% | +16.00% | -13.60% | -2.30% | +17.50% |

Taken together, these relative shifts position the 60/40 with a 20% ADT overlay as the strongest configuration tested. The annualized return improves by 15%, with cumulative performance higher by 19%, while the risk profile also strengthens: Sharpe increases 16%, volatility is reduced, and the maximum drawdown improves by almost 14%. Once again, the negative skew is decreased by over 17%, reflecting ADT’s contribution to positive volatility. Overall, the combination provides the most effective enhancement to both absolute and risk-adjusted outcomes when incorporating a truly non-correlated alternative.1

In our view, this approach offers the most compelling way to introduce a non-correlated alternative and enhance both absolute and risk-adjusted outcomes. To discuss how true alternatives can be integrated into your portfolio or client offering2, reach out to us at info@auspicecapital.com

For more information on the Auspice One Fund, including structure (i.e., $2 of exposure per $1 of invested capital – $1 of S&P 500 and $1 of ADT diversifier), performance, and additional materials, visit our fund page here.

Foot Notes

1 There is no assurance that these historical or hypothetical improvements will be achieved in the future, and outcomes may vary based on market conditions, timing, rebalancing methodology, and other factors.

2 Before investing in any Auspice-managed product, investors should review the applicable simplified prospectus or offering document, which contains important information about risks, fees and strategy-specific considerations.

DEFINITIONS

Indices

Indices and benchmarks are used for comparison purposes only or to illustrate comparisons against other widely used indices or benchmarks most commonly referenced by investors. Index statistics/data are sourced from Bloomberg. You cannot invest directly in an index.

Bloomberg U.S. Agg Total Return Index (LBUSTRUU Index) – is a benchmark that tracks the U.S. investment-grade, fixed-rate, taxable bond market, including U.S. Treasuries, government-related, corporate, asset-backed, and mortgage-backed securities. It is widely used to gauge the performance of the overall U.S. bond market, and its total return value reflects both price changes and income from coupons.

Bloomberg All Hedge Fund Index (BHEDGE Index) – represents the average performance of hedge funds, as defined by the Bloomberg Hedge Fund Classifications. Constituents and weights may change over time, and the index is subject to survivorship, self-reporting and selection biases. The index is non-investable and intended only as a general industry indicator.

Auspice Managed Funds - Auspice Diversified Trust (ADT) and Auspice One Fund Trust (AOFT) are investment funds managed by Auspice Capital Advisors Ltd. Information relating to these funds is provided for illustration only. Commissions, management fees, and expenses may be associated with these funds. Please read the simplified prospectus before investing.

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. Hypothetical performance results are generally prepared with the benefit of hindsight and do not involve financial risk. No hypothetical performance record can completely account for the impact of financial risk in actual trading. There are numerous other factors related to the markets in general or to the implementation of any specific trading program that cannot be fully accounted for and that can adversely affect actual trading results.

The hypothetical performance shown does not reflect the deduction of advisory fees, trading commissions or other expenses that would be incurred in an actual account.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus or applicable offering document before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

These materials are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. (the “Manager” or “Auspice”) makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the applicable offering documents before investing.

This material may contain forward-looking statements, which were prepared for the purpose of providing general educational background information and may not be appropriate for other purposes. Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to an Auspice managed investment fund (the “Fund”), where applicable, and the Manager. Forward- looking statements are not purely historical facts but reflect the current expectations of the Fund, where applicable, and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s, where applicable, and the Manager’s current, reasonable beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund, where applicable, and the Manager believe to be reasonable, neither the Fund, where applicable, or the Manager can assure investors that actual results will be consistent with these forward-looking statements. There is no guarantee that any forward-looking statement will come to pass. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

Neither the Fund, where applicable, nor the Manager assumes any obligation to update or revise any forward-looking statement to reflect new events or circumstances, except as required by law.

The Manager may present the enclosed information in a blog – such blog may contain hypertext links to web sites owned and controlled by parties other than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on such web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.