To download the Auspice December Blog as a PDF, click here.

This expanded version of Tim Pickering’s special to the Financial Post presents a detailed 2026 outlook for commodity markets and the forces reshaping them. It examines how years of underinvestment in supply, combined with structural demand drivers such as electrification, deglobalization, and evolving agricultural dynamics, are shaping opportunities across the commodity complex. In this context, commodities are positioned as the most diverse asset class with the potential to enhance diversification and portfolio resilience as macro conditions continue to shift.

This commentary reflects the views of the author and is provided for informational and educational purposes only. It discusses market conditions and indices and may reference forward-looking statements. It does not constitute investment advice or a recommendation. Please see the Important Disclaimers and Notes section below for full details.

I started my career at a Canadian bank in 1995. As the ‘90s came to an end, markets were driven by the “dot-com” boom and the technology surrounding the internet. However, I chose another path: commodity markets. At the time, my colleagues and even family thought I was crazy. Commodities had broadly languished, and this new technology was clearly a game changer. While I was too green to realize it at the time, the first ingredient for a commodity supercycle was already in place. The world had spent years underinvesting in supply, and capital expenditure (Capex) remained low. However, this in itself does not cause the cycle. You need demand, more accurately, a generational demand shock. Entering the new millennium, that shock hit – China. Its development, industrialization and rapidly growing middle class were the drivers, and supply struggled to keep up for the next decade.

As we entered the 2020s, COVID hit while the commodity setup quietly took shape in the background. Capex peaked broadly in commodities circa 2012-14, then softened, and remains below those levels. On the demand side, we believe there haven’t been as many significant commodity drivers since industrialization and post-WW2. There isn’t just one factor like China in the 2000s cycle; there are many (illustrated in Figure 5).

Our 2026 outlook is shaped by these drivers and additional macro themes, each a meaningful game changer.

While Gold’s performance since 2023 has been outstanding, it has not behaved as a traditional inflation hedge (its move began AFTER inflation had already moderated back toward the U.S. CPI’s 100-year average of 3%), nor does it represent commodities broadly. In our framework, Gold does not currently meet the criteria at present to be top of our macro list. We believe its recent drivers are more closely tied to sentiment than to the cycle drivers we will explore. In this way, it resembles Bitcoin and has traded in a similar fashion since 2020.

AI and Electrification

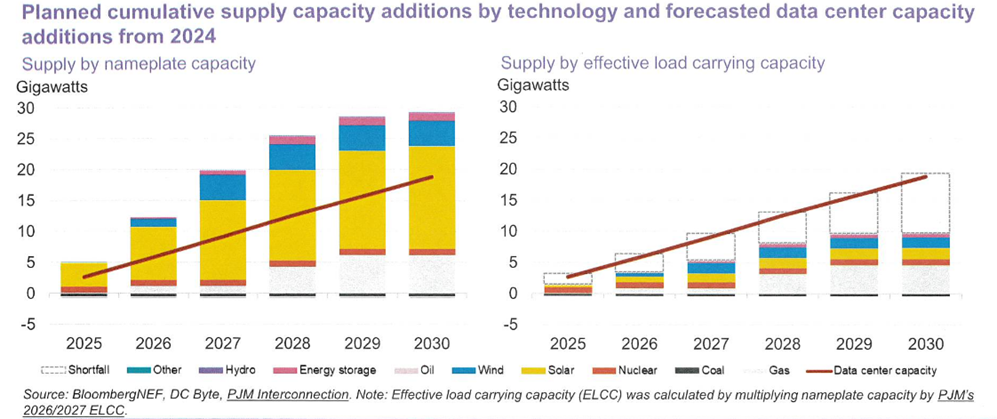

The first theme is undeniable. AI and data centers are not just about semiconductors - it is about electrification and building the infrastructure it requires. Its energy needs are broad and massive, as displayed in Chart 1. To borrow a line we couldn't write any better: "Like all technologies known to man, AI has a dark side to it: high energy consumption." The demand for power by hyperscalers means more development, and as Reuters highlights, "access to electricity is not keeping up." The build-out requires energy, yet with soft 2025 prices, one could argue that this demand is being ignored. In fact, the IEA has warned that global energy security faces “overlapping risks as demand surges, supply chains weaken, and electrification accelerates”. Its recent World Energy Outlook report expanded to include electricity grids, critical minerals and infrastructure. As such, the related commodity demand has widened from the obvious markets, being copper and power, to include all energy sources, including petroleum, natural gas and uranium.

Chart 1 – PJM Data centers outpace effective Supply Additions Through 2030:

Source: BloombegNEF

AI and electrification eat commodities. We require the construction machines that run on these fuels to build the infrastructure. The physical infrastructure itself requires vast amounts of iron ore (steel) and aluminum. EVs and renewables add further demand for lithium, cobalt, tin, nickel, and zinc in addition to platinum and palladium. Look for these markets to provide opportunities beyond those seen recently in Gold and Silver.

Deglobalization

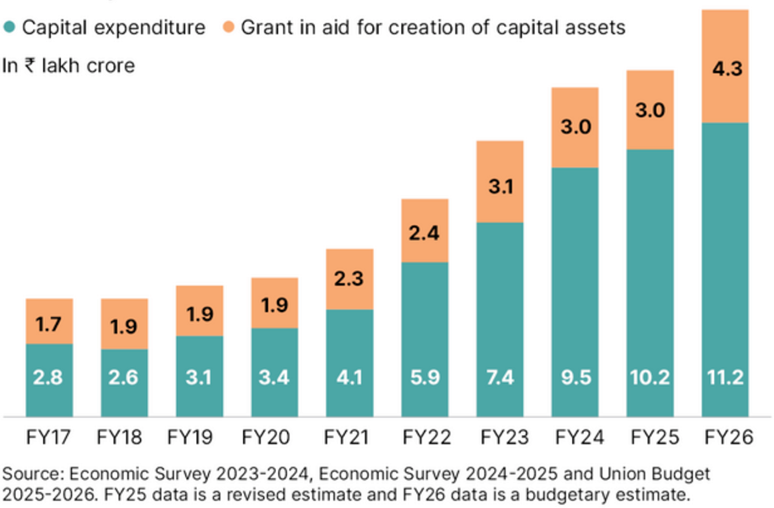

The shift to deglobalization has largely been blamed on Trump’s protectionist tariff policies. However, this is not an equitable explanation - this trend has been underway for a long time. Rising nationalism and populism are not new for two of the largest commodity consumers, China and India. In fact, as shown in Figure 2, India has more than tripled its infrastructure Capex since 2019, alongside commodity export bans including wheat, rice, and sugar. This comes as supplies are tight in markets like Sugar. We believe India could emerge as the world’s largest commodity consumer, with its middle class set to surpass that of the US and China in size, guided by a different playbook.

Figure 2: Capital Outlay and Grants for Asset Creation in India

Source: Value Research

The overall effect of deglobalization is volatility and regional price squeezes in largely similar markets. For example, Wheat in North America can behave differently than in Europe or Africa. That divergence creates opportunities for commodity trading advisors and managers like Auspice, who look globally. For investors, looking beyond headline markets is prudent.

Agricultural Markets

The Ag sector, namely Grains and Soft Commodities, has provided some incredible opportunities in recent years across a broad range of markets. We have seen big trends in Softs such as Coffee, Cocoa, Sugar and Orange Juice. But something has been forgotten.

While the world keeps growing (and eating), grain prices remain near all-time lows. This is at odds with the high and rising costs of farmland, labour, fertilizer, and machinery (driven by metals and energy) highlighted in Figure 3.

Figure 3: US Food Production Costs Have Broken Away from Crop Prices

Source: USDA QuickStats & Bloomberg. Agricultural Input Cost represents an aggregate YoY % change in farmland, labour, fertilizer, fuel, and machinery costs.

Given global growth-driven demand, deglobalization and shipping issues, we believe Grains may provide a significant opportunity in the future. This may benefit different geographic markets in Wheat, Corn, Soybeans and Canola

Signs of Change

We see two main signs of change.

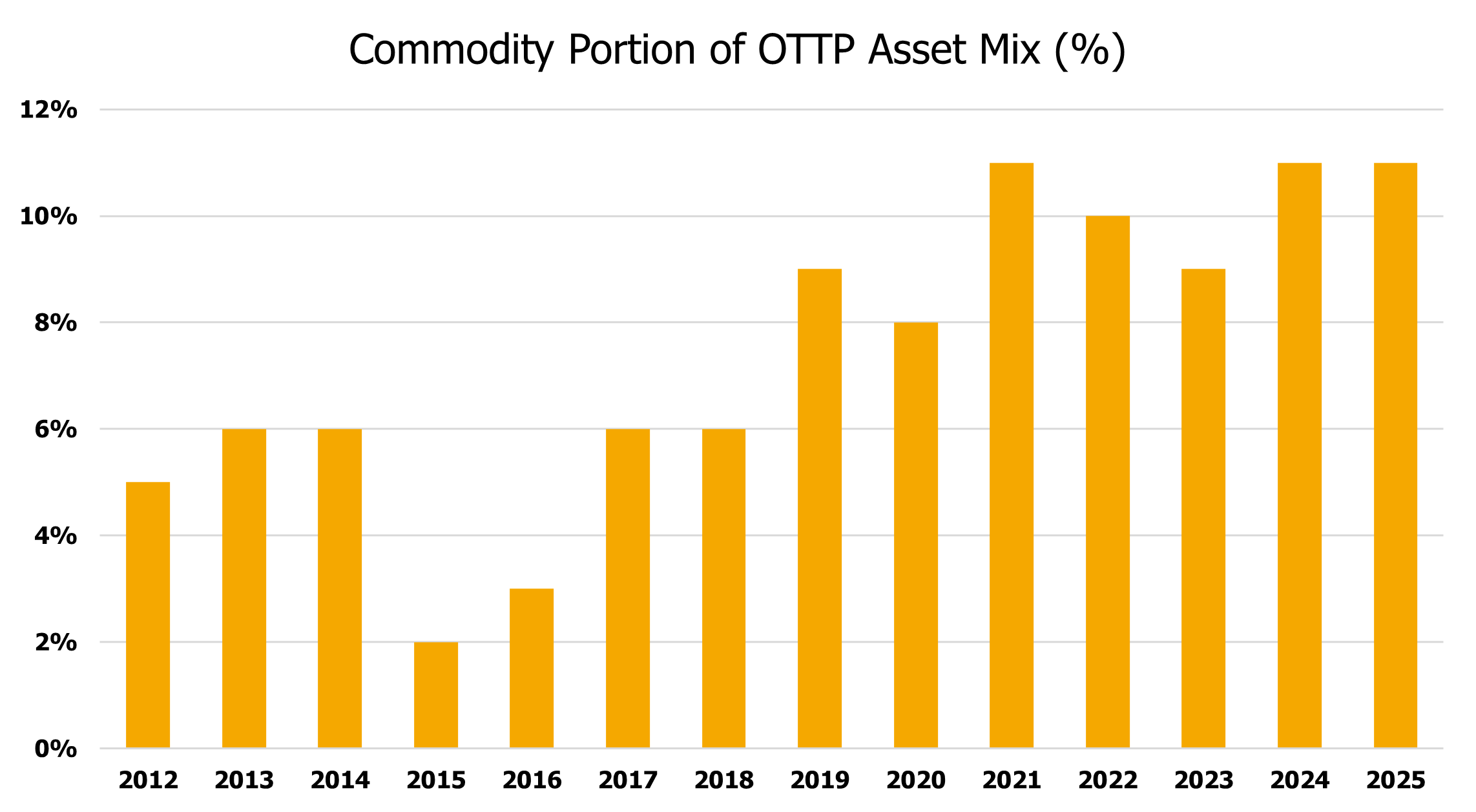

First, while commodities have been under-allocated for the past decade, there is an observable shift. Historically, pensions held 15-20% in commodity exposure. This dropped to almost nothing post-2012. The commodity cycle peaked, and quantitative easing alongside zero inflation enabled bonds to hedge heavy equity exposure. However, in a normal inflation world like pre-2000, bonds don’t hedge equities, and allocations are returning to commodities. Industry leader Ontario Teachers is a clear example, currently holding an 11% direct commodities allocation (up from 5% in 2012) as shown in Figure 4. This may signal a broader reassessment of commodity allocations among institutional investors.

Figure 4: OTPP Commodities Allocation Growth Since 2012

Source: Ontario Teacher’s Pension Plan & Auspice Capital Operations

Second, sanctions, conflicts, and supply disruptions are pushing commodity shipping rates - from energy to bulk ores and grains - towards a rare year-end surge. This potentially upends global supply chains at a time of deglobalization, AI/electrification demand, and cheap Ag markets. While we have no crystal ball, this is often a leading indicator of commodity volatility and demand.

Summary

It remains in the US central bank’s best interest, alongside its “pro-growth at all costs” government, to avoid stagflation and change the narrative to a reality: we do not believe 2% US CPI is on the horizon any time soon - society, business, and governments should be happy at the average zone (3-4%) with a strong and growing economy. It has increasingly become clear that inflation is cost-push driven (wages and inputs/commodities), recognizing that commodity prices continue to rise. Commodities have historically served as a valuable diversifier in periods of inflation (normal or elevated) and high equity valuation.

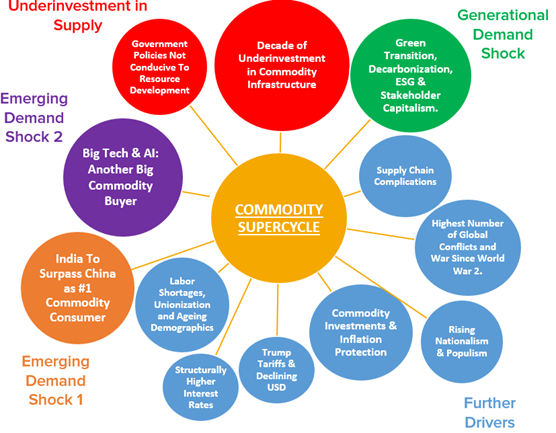

Commodities are the most diverse asset class, far beyond the headline markets. After moderating post-rally into 2023, commodities have more broadly woken up and provided trends in 2025. This comes on the back of what we see as early days of a potential longer-term commodity supercycle, which historically has lasted more than 10 years. We believe it may be longer, given the prolonged time required to bring new supply into production due to government policies that are not conducive to resource development, particularly in the Western world. See Figure 5 at 11 o’clock. This is supported by strong fundamentals, considerable demand, and exacerbated by themes we have identified here, in addition to the myriad of other factors affecting the commodity cycle.

Figure 5: 2020s Cycle Drivers

Source: Auspice Capital Advisors

Commodities demand your attention. For investors considering portfolio construction, this may be an opportune time to evaluate diversification beyond recent equity strength, including the role of tactical commodity strategies managed with discipline and experience.

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results. The views expressed are those of the author and do not constitute investment advice.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus or applicable offering document before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

These materials are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. (the “Manager” or “Auspice”) makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the applicable offering documents before investing.

This material may contain forward-looking statements, which were prepared for the purpose of providing general educational background information and may not be appropriate for other purposes. Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to an Auspice managed investment fund (the “Fund”), where applicable, and the Manager. Forward- looking statements are not purely historical facts but reflect the current expectations of the Fund, where applicable, and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s, where applicable, and the Manager’s current, reasonable beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund, where applicable, and the Manager believe to be reasonable, neither the Fund, where applicable, or the Manager can assure investors that actual results will be consistent with these forward-looking statements. There is no guarantee that any forward-looking statement will come to pass. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

Neither the Fund, where applicable, nor the Manager assumes any obligation to update or revise any forward-looking statement to reflect new events or circumstances, except as required by law.

The Manager may present the enclosed information in a blog – such blog may contain hypertext links to web sites owned and controlled by parties other than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on such web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.