Auspice Managed Futures Excess Return Index (AMFERI)

Market Review

The AMFERI had a great April as volatility picked up in both financial and commodity sectors alike. While across all global assets, much of the opportunity came from the equity markets, an area not included in this strategy, the index continued to find tactical value in less obvious places. The month was dominated by the Metals market. The portfolio composition and agility is a central feature of the strategy and its intention to provide non-correlation to institutional and retail equity biased portfolios.

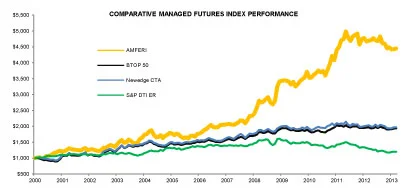

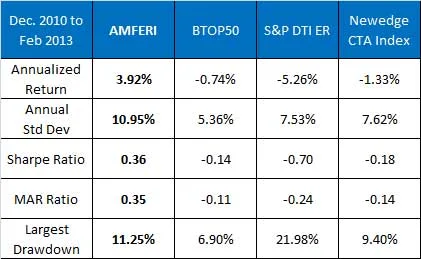

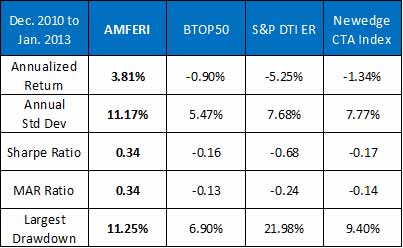

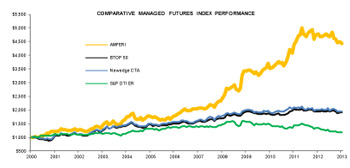

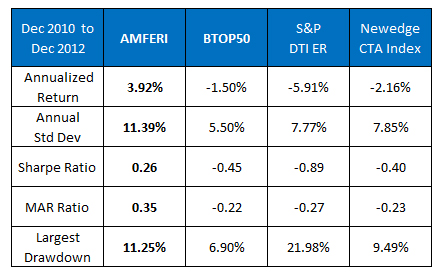

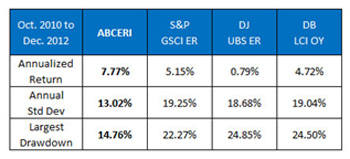

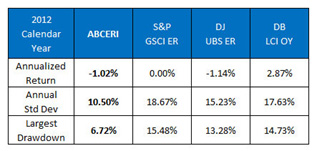

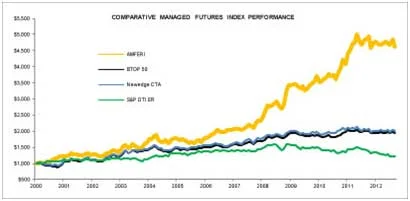

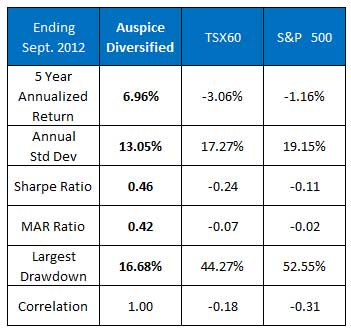

As seen in the next table, the performance of AMFERI versus both investable and non-investable managed futures indices has been good. Since the launch of the index in December 2010, AMFERI continues outperform on both an absolute and risk-adjusted basis.

After a period of challenge for many managed futures strategies, the index is off to a strong start in 2013 making back a significant part of the recent modest drawdown. Pullbacks happen within all strategies; however with managed futures such drawdowns can be an opportune time for investors. Investors should consider the drawdown history of their preferred strategy and gain expectations for potential payoff on recovery and extension.

For those interested in a copy of an analysis of the drawdown and recovery periods for AMFERI, please contact Auspice. See synopsis to the right.

SYNOPISIS OF DRAWDOWN ANALYSIS

Managed Futures is typically a difficult strategy to time because of the non-correlated performance that results from the widespread diversification of market sectors covered. One of the best ways to consider an entry point is through an understanding of drawdowns over time. Pullbacks occur in every strategy, however given transparency of the returns, it is intuitive to analyze the character of the pullbacks and subsequent gains with managed futures. These pullbacks generally represent an opportunity from which trends develop and extend. Furthermore, the time to make new gains is often quicker than the length of the pullback (peak to valley).

Please contact us at info@auspicecapital.com for the complete analysis.

Index Review

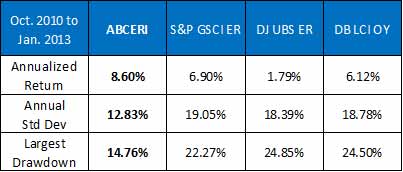

The AMFERI was up 2.27% in April and is up 3.95% (table below) in 2013, outperforming a number of investable and non-investable CTA indices highlighted in the table.

Portfolio Recap:

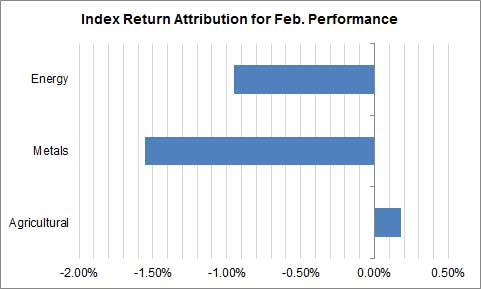

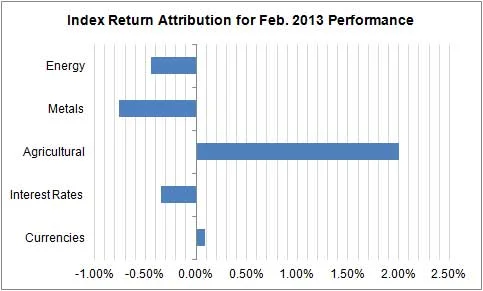

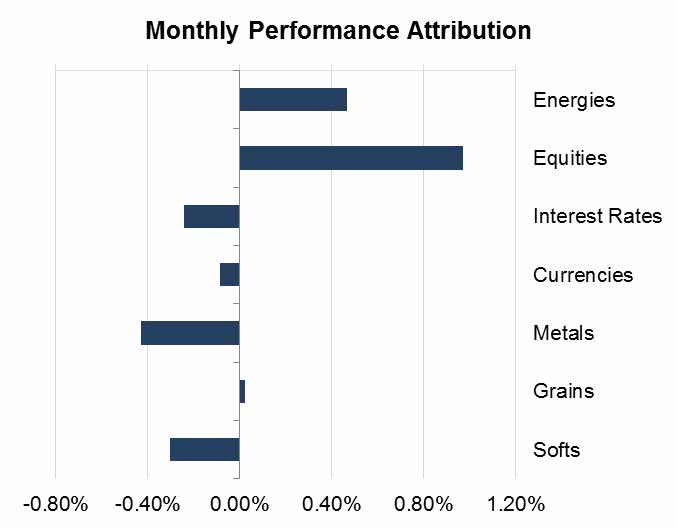

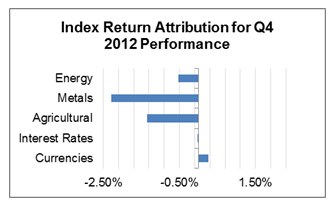

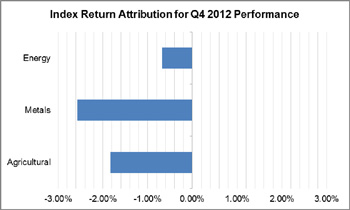

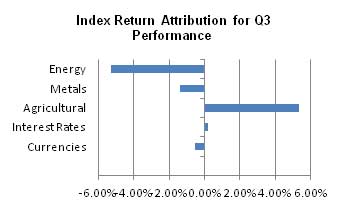

In April the index was up in 1 of the 5 sectors. The strongest sector was Metal. The top performing components within the index were shorts in Gold, Silver and Copper complimented by Corn, Crude and Sugar. Long gains were made in Natural Gas. The most challenging sector was Ags after having a very strong March on the short side. The index is currently positioned short in 10 of 12 commodity markets and a number of positions changed intra-month. The index is also tilted long in the financial markets with 5 of the 9 components holding a long weight. Within Financials, Currencies remain a balanced short and long (3 and 3). Interest rates components are mixed with a move to long in 2 of the 3 markets as the price trend pushed higher.

In April the index was up in 1 of the 5 sectors. The strongest sector was Metal. The top performing components within the index were shorts in Gold, Silver and Copper complimented by Corn, Crude and Sugar. Long gains were made in Natural Gas. The most challenging sector was Ags after having a very strong March on the short side. The index is currently positioned short in 10 of 12 commodity markets and a number of positions changed intra-month. The index is also tilted long in the financial markets with 5 of the 9 components holding a long weight. Within Financials, Currencies remain a balanced short and long (3 and 3). Interest rates components are mixed with a move to long in 2 of the 3 markets as the price trend pushed higher.

Energy

The petroleum weights have now tilted short – as we have added short positions in Gasoline and Heating Oil while holding short Crude Oil. The index has also moved Natural Gas to a long position for only the second time in 5 years. This was a month of transition for the Energy Sector and the sector was a negative contributor on the month.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and benefitted from the significant weakness in Gold and Silver and to a lesser degree Copper. All metals bounced back at month end but remained sharply lower.

Agriculture

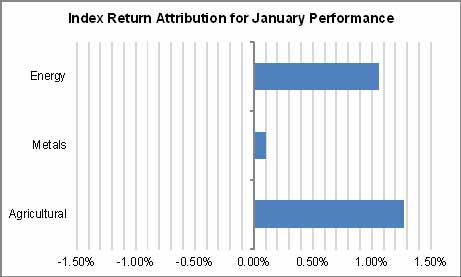

While Ags did very well on the short side in March, most markets corrected in April. Grains moved higher with the exception of Corn and Sugar which continued to drift lower. Cotton remains the lone long position in the sector but was pushed lower for a loss.

Interest Rates

After recently moving all components to take advantage of higher interest rates (short bonds), 2 of the 3 markets have gone long. This is on the back of strong renewed momentum higher in rate futures. The index switched both US 5 year and 10 year Notes to long while remaining short 30 year long bonds. There was a small loss from this sector as positions transitioned on the higher price movement.

Currencies

Currencies were flat in April and position weights remain the same. Small gains were made remaining short the Japanese Yen and long the Euro. Most other markets lacked significant short term trend and we remain positioned with the long term trend. We are long Aussie dollar and US Dollar Index while short the British Pound and the Canadian dollar at this time.

Outlook

The AMFERI was up in Q1 and had a strong start to 2013 alongside the equity market despite a lack of equity exposure in the portfolio. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in April, the sharp sell-off and correction highlight the volatility and risk of the sector. Not all equity markets were up. Many equity markets, including small caps and country specific markets like Canada were lower on the month. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear. Managed Futures and the AMFERI are a good way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in April through our shorts in Metals.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.

The petroleum weights have now tilted short – as we have added short positions in Gasoline and Heating Oil while holding short Crude Oil. The index has also moved Natural Gas to a long position for only the second time in 5 years. This was a month of transition for the Energy Sector and the sector was a negative contributor on the month.

The Energy sector remains choppy with an overall negative bias to trend in the petroleum components.

Metals

The Metals sector remains short and benefitted from the significant weakness in Gold and Silver and to a lesser degree Copper. All metals bounced back at month end but remained sharply lower.

Agriculture

While Ags did very well on the short side in March, most markets corrected in April. Grains moved higher with the exception of Corn and Sugar which continued to drift lower. Cotton remains the lone long position in the sector but was pushed lower for a loss.

Interest Rates

After recently moving all components to take advantage of higher interest rates (short bonds), 2 of the 3 markets have gone long. This is on the back of strong renewed momentum higher in rate futures. The index switched both US 5 year and 10 year Notes to long while remaining short 30 year long bonds. There was a small loss from this sector as positions transitioned on the higher price movement.

Currencies

Currencies were flat in April and position weights remain the same. Small gains were made remaining short the Japanese Yen and long the Euro. Most other markets lacked significant short term trend and we remain positioned with the long term trend. We are long Aussie dollar and US Dollar Index while short the British Pound and the Canadian dollar at this time.

Outlook

The AMFERI was up in Q1 and had a strong start to 2013 alongside the equity market despite a lack of equity exposure in the portfolio. Consider this fact as one looks for opportunities to reduce portfolio risk given the traditional markets have performed well in the last couple of years.

While the broad equity market ended higher in April, the sharp sell-off and correction highlight the volatility and risk of the sector. Not all equity markets were up. Many equity markets, including small caps and country specific markets like Canada were lower on the month. While we don’t have crystal ball, consider ways to protect the portfolio as cracks start to appear. Managed Futures and the AMFERI are a good way to add non-correlation and portfolio protection, while still having absolute return from tactical exposures as we saw in April through our shorts in Metals.

Strategy and Index

The Auspice Managed Futures Index aims to capture upward and downward trends in the commodity and financial markets while carefully managing risk. The index will use a quantitative methodology to track either long or short positions in a diversified portfolio of 21 exchange traded futures which cover the energy, metal, agricultural, interest rate, and currency sectors. The index incorporates dynamic risk management and contract rolling methods. The index is available as either a total return index (includes a collateral return) or as an excess return index (no collateral return).

About the Index Provider

Auspice is an innovative asset manager that specializes in applying formalized investment strategies across a broad range of commodity and financial markets. Auspice’s portfolio managers are seasoned institutional commodity traders. Their experience, trading one of the most volatile asset classes, forms the backbone of their strategy for generating profits while preserving capital and dynamically managing risk. Auspice Capital Advisors Ltd. is a registered Portfolio Manager / Investment Counsel / Exempt Market Dealer in Canada and a registered Commodity Trading Advisor (CTA) and National Futures Association (NFA) member in the US.

Auspice’s core expertise is managing risk and designing and executing systematic trading strategies. Auspice uses its diverse trading and risk management experience to manage 4 diverse product lines. and has been described as a “next generation CTA”, offering strategies in active managed futures (CTA), passive ETFs, enhanced indices and custom commodity strategies.